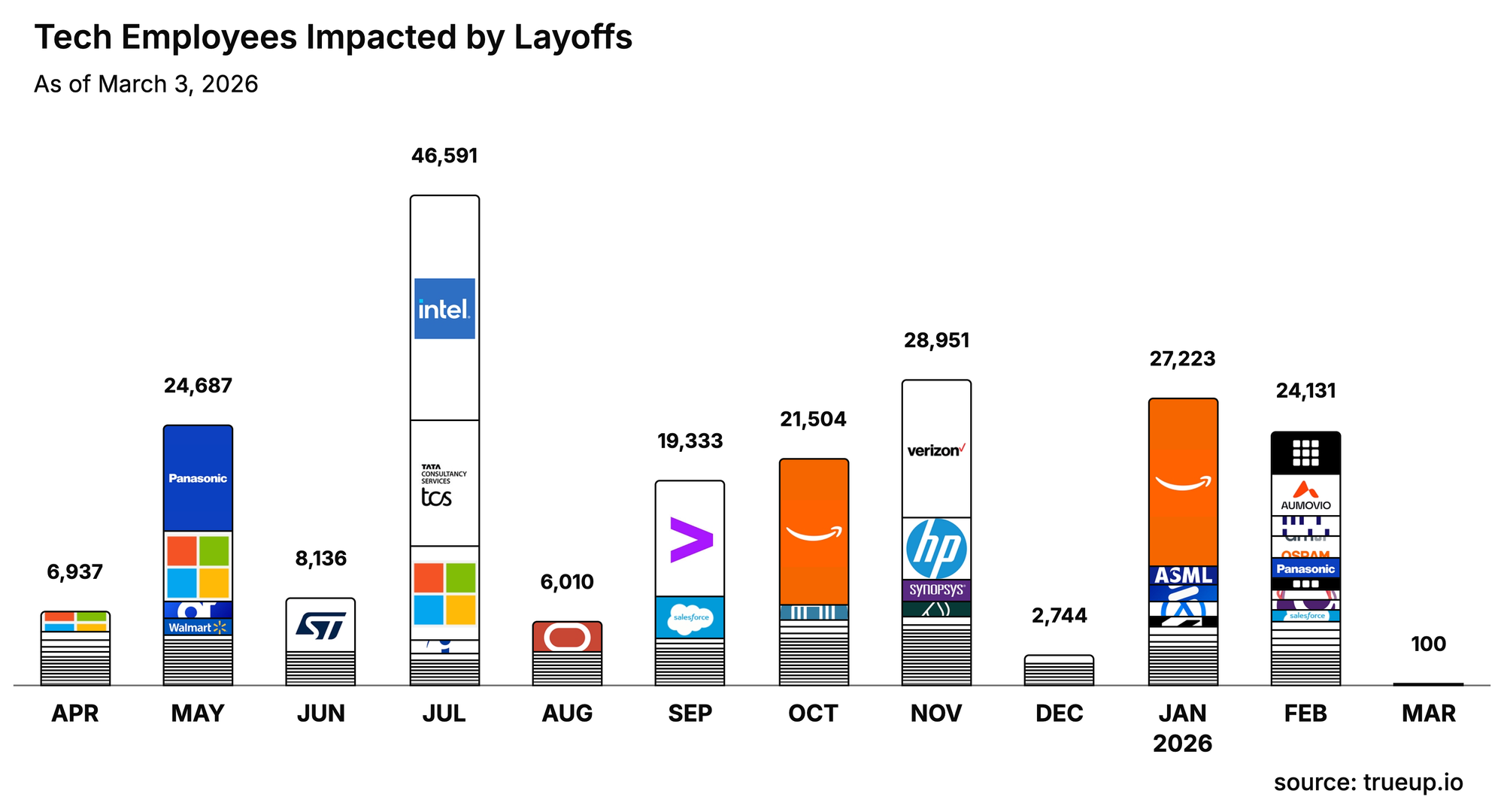

In the first two months of 2025, the technology industry shed more than 30,000 jobs, according to data tracked by Layoffs.fyi.

The roster of companies making those announcements reads like a directory of Silicon Valley's most recognizable names: Microsoft, Google, Salesforce, Workday, Okta, and a lengthening list of mid-size software companies that had quietly overhired during the post-pandemic boom.

Every significant wave of tech layoffs arrives with its own narrative framework. In 2022, it was "macroeconomic headwinds." In 2023, companies leaned on the language of "right-sizing." In 2025, the dominant explanation, stated explicitly in some cases and implied in many others, is artificial intelligence.

The message being communicated to investors, to the press, and sometimes directly to departing employees is consistent: AI is restructuring what work requires, certain job functions are being absorbed by automation, and leaner teams represent the future of how software companies operate.

The question worth asking, with some rigor, is whether that explanation is accurate, and to what extent it is serving as convenient cover for decisions rooted in entirely different pressures.

The Numbers Behind the Headlines

Before drawing conclusions, the underlying data deserves a careful reading, because not all layoff waves are structurally identical.

Layoffs.fyi tracked roughly 32,000 publicly disclosed job cuts between January 1 and late February 2025. That figure represents a meaningful acceleration relative to the same period in 2024, though it remains well below the historic peaks of early 2023, when more than 90,000 workers were let go in a single month following the interest rate shock that repriced the entire growth-tech sector.

What distinguishes the current wave is not its scale but its context. These are not companies under financial duress.

| Company | Action | Financial Context |

|---|---|---|

| Microsoft | ~1,900 gaming division cuts | Reported record $62B quarterly revenue days later |

| Salesforce | Several hundred roles trimmed | Simultaneously promoting Agentforce as a labor replacement |

| Multiple restructuring rounds over 18 months | Targeting teams whose functions overlap with internal AI tooling | |

| Workday | Significant headcount reductions | Announced concurrent AI product investment strategy |

That pattern, headcount reduction running in parallel with high-profile AI investment, is the engine driving the dominant narrative. The simultaneity of these two trends does not establish causation, however, and the picture requires considerably more careful analysis to understand which force is actually doing the most work.

Where AI Is Genuinely Reshaping Headcount

There are specific job categories where the automation story is not only credible but backed by observable, documented patterns rather than executive messaging. Identifying these areas clearly matters precisely because conflating them with layoffs driven by other factors muddies the broader analysis.

Customer Support and Service Operations

Customer support is arguably where AI displacement is most concrete and most measurable right now.

Klarna generated significant press coverage when its CEO Sebastian Siemiatkowski claimed the company's AI assistant was performing the work of 700 customer service agents. That figure was widely disputed and almost certainly inflated, but the structural trend it points to is real: conversational AI systems built on large language model infrastructure have meaningfully reduced the per-ticket labor cost of customer support at scale.

Zendesk, Intercom, and Salesforce's Service Cloud have each shipped AI capabilities that allow smaller support teams to manage substantially higher ticket volumes without proportional staffing increases. The economic logic is straightforward: if a well-configured AI system can autonomously resolve 40 to 60 percent of inbound queries, the marginal cost of scaling support drops significantly. For companies running large operations, that arithmetic eventually translates into headcount decisions.

Software Quality Assurance and Testing

QA engineering has been under quiet but persistent pressure for longer than most industry observers have acknowledged, and the current AI wave has accelerated a trend already underway.

Automated testing frameworks predate generative AI by many years, but the latest generation of AI-assisted platforms, including tools from Mabl and Testim along with GitHub Copilot's expanding capacity for test generation, has materially reduced the manual labor involved in regression testing, edge case identification, and bug verification.

The impact is concentrated at the junior end of the QA career ladder, where roles are being eliminated outright or, more commonly, not backfilled when vacancies arise. Senior engineers capable of designing complex test architectures and interpreting nuanced system behavior remain in demand, but the entry-level pipeline is narrowing at companies that have adopted AI-assisted tooling in any meaningful capacity.

Entry-Level Content and Copywriting

Marketing departments that previously employed cohorts of junior writers to produce product descriptions, advertising copy, email sequences, and SEO-targeted content have been among the earliest and most visibly affected groups.

Generative AI has made it practically feasible for a single experienced content strategist to produce output volumes that previously required a team of three or four, particularly for templated, high-frequency, or data-driven content categories.

This does not mean the resulting content is superior. In many measurable respects, it demonstrably is not, particularly in terms of originality, brand voice consistency, and the kind of nuanced audience understanding that experienced writers develop over time. The quality tradeoff is real and increasingly recognized. Nevertheless, the cost calculus has shifted enough that organizations are making staffing decisions accordingly, often before fully accounting for the downstream quality implications.

Where AI Is Being Used as Narrative Cover

The more important and underexamined dimension of the current layoff cycle is the degree to which AI is functioning as a rhetorical device rather than an operational reality, allowing companies to reframe financial restructuring as technological evolution.

A substantial portion of the cuts occurring right now have very little to do with AI absorbing specific job functions. They reflect, instead, a broader and long-overdue recalibration of what institutional investors expect from public technology companies in an environment where the cost of capital has permanently increased relative to the zero-rate era that shaped hiring decisions between 2019 and 2022.

The extraordinary hiring expansions of that period, fueled by near-zero interest rates, pandemic-accelerated digital adoption, and abundant venture capital, produced organizational structures that were never designed to operate efficiently at normal growth rates. When the Federal Reserve's rate cycle repriced growth-oriented equities in 2022, companies that had doubled or tripled their headcount found themselves under structural pressure to demonstrate operating leverage they had not previously been required to show. The adjustment was delayed, partial, and often managed in stages, which is part of why the correction is still playing out in 2025.

Cutting 5 to 8 percent of a workforce while announcing a concurrent AI investment strategy accomplishes two things that are individually valuable but become particularly powerful in combination:

- It reduces the payroll burden that has been suppressing operating margins

- It reframes the reduction as a proactive, forward-looking transformation rather than a reactive course correction

"We are investing in AI and building for the next era" is a considerably more compelling earnings call narrative than "we over-hired between 2020 and 2022 and are now correcting that error."

Bernstein Research published commentary in late 2024 making this dynamic explicit, observing that a meaningful number of enterprise software companies were using AI investment announcements as narrative scaffolding around what were, structurally, straightforward efficiency-driven restructurings.

The workers being cut in these cases are frequently not in roles that AI has displaced at all. They tend to fall into one of three categories:

- Middle management layers that accumulated during rapid growth but whose coordination functions have since diminished

- Redundant program management roles created to serve organizational complexity that no longer exists at the same scale

- Operational support positions built for headcount levels the company no longer intends to maintain

The Salesforce Agentforce Question

Salesforce occupies a distinctive position in this conversation because it is one of the very few companies willing to make a direct, public argument that its own AI product is actively responsible for internal workforce decisions.

CEO Marc Benioff has been consistent and unusually specific in his advocacy for Agentforce, the company's autonomous AI agent platform, and what it is capable of executing across sales workflows, service operations, and back-office functions. In his January earnings commentary, Benioff suggested that Agentforce was managing tasks that would previously have required dedicated human workers, and indicated that this operational reality was informing how Salesforce was thinking about its own organizational structure.

That is a notable claim for several reasons. It represents a company explicitly modeling its internal workforce planning around the capabilities of technology it both develops and deploys commercially. There is an inherent complexity in that position:

- Benioff has strong incentives to demonstrate Agentforce's transformative potential to the market

- Those incentives are not entirely separable from the claims being made about its internal impact

- Whether Agentforce has genuinely displaced a meaningful number of Salesforce employees, or whether the framing reflects an aspirational narrative as much as documented operational reality, is difficult to verify from outside the organization

What is not in doubt is that Salesforce is building its entire product roadmap around the premise that AI agents can execute a substantial and growing portion of white-collar knowledge work with minimal human intervention. If that strategic bet proves directionally correct over a three-to-five-year horizon, the workforce implications extend well beyond any single company's restructuring decisions, touching the entire enterprise software ecosystem and the millions of knowledge workers whose job functions overlap with what Agentforce and competing platforms are designed to perform.

What the Research Actually Shows

Setting aside the narratives that individual companies are constructing, the academic and institutional research on AI's impact on employment presents a picture that is genuinely complex and, in several important respects, at odds with both the most alarmist and the most dismissive positions in the public debate.

| Research Source | Key Finding | Implication |

|---|---|---|

| MIT CSAIL, 2024 | Full automation is economically unattractive for a significant share of tasks, despite technical feasibility | The gap between what AI can do and what makes financial sense to automate is larger than commonly assumed |

| Goldman Sachs | Generative AI could automate 25 to 30% of U.S. work tasks over the next decade | Task-level disruption spread over time, not sudden elimination of entire job categories |

| Stanford HAI / McKinsey | Accelerating AI adoption in enterprise settings throughout 2024, concentrated in data analysis, content, and code review | AI is measurably reshaping specific roles, but adoption remains uneven |

The MIT finding most people miss

A 2024 paper from MIT's Computer Science and Artificial Intelligence Laboratory examined the economic viability of AI automation across a broad range of job tasks and arrived at a finding that receives insufficient attention in mainstream coverage.

Despite the technical feasibility of automating many knowledge-work functions, the cost structure of deploying AI systems at scale makes full automation economically unattractive for a significant proportion of them. The implication is that the gap between what AI can theoretically do and what it makes financial sense to automate is larger than the prevailing narrative acknowledges, particularly for tasks requiring substantial contextual judgment or where the cost of errors remains high.

What Goldman Sachs is actually saying

Goldman Sachs has estimated that generative AI could automate 25 to 30 percent of work tasks across the U.S. economy over the coming decade. That is a substantial figure in aggregate, but it is important to understand what it is actually measuring: task-level automation potential spread across a long timeframe, not the sudden elimination of discrete job categories.

Much of the projected automation would manifest as a reduction in time spent on specific activities within broader roles, potentially shifting the nature of work without eliminating the positions themselves.

Where acceleration is documented

Stanford's Human-Centered AI Institute and the McKinsey Global Institute both documented accelerating AI adoption in enterprise environments throughout 2024, with particular concentration in knowledge-work tasks involving data analysis, written content generation, and code review. Those adoption patterns do support the argument that AI is beginning to reshape the practical content of certain roles in measurable ways.

The responsible synthesis of the available evidence is this: AI is creating genuine, task-level disruption in specific and identifiable domains. The displacement is real but concentrated rather than broad-based, and it is occurring alongside, rather than independently of, the financial and structural pressures that are the primary drivers of the current layoff cycle.

The Roles Most Exposed Over the Next Three Years

For professionals attempting to assess their own career exposure, the picture varies considerably depending on the specific nature of the work, the degree to which it involves routine tasks with measurable outputs, and the extent to which contextual judgment or creative synthesis is central to the role's value.

| Role Category | Near-Term Risk | Primary Reason |

|---|---|---|

| Tier-one customer support | High | Conversational AI now resolves a significant share of routine queries autonomously |

| Data entry and processing | High | Repetitive, well-defined tasks are the most economically viable targets for automation |

| Templated content writing | High | Generative AI matches output volume at a fraction of the labor cost |

| Basic financial reconciliation | High | Rule-based workflows are tractable for current AI tooling |

| Junior software QA | High | AI-assisted testing platforms reduce the manual labor floor substantially |

| Senior engineering and architecture | Low | Complex system reasoning and judgment still require human expertise |

| Strategic and executive roles | Low | Multi-stakeholder judgment, organizational context, and relational capital remain difficult to automate |

| Sales and account management | Moderate | Routine outreach and reporting face automation; relationship-driven work does not |

| Creative direction and brand strategy | Low to Moderate | AI can generate volume, but not reliably produce differentiated, high-stakes creative judgment |

The subtler threat: workforce compression

The more consequential risk may not be outright elimination but workforce compression. AI tools enable a smaller number of people to produce what previously required a larger team, which translates into slower hiring rather than dramatic displacement events.

This mechanism is harder to observe in headline layoff figures, but over a multi-year horizon it may have a larger cumulative effect on employment levels and wage dynamics than any individual round of announced cuts.

Why the Framing Matters Beyond the Optics

The question of whether AI is the primary driver of current layoffs or primarily a convenient narrative frame is not merely a matter of intellectual accuracy. The answer carries meaningful policy and institutional implications that will shape how workers, governments, and companies navigate the transition that is genuinely underway.

If AI displacement is the primary driver, the appropriate institutional response involves:

- Sustained investment in retraining infrastructure and skills transition programs

- Structural reform of unemployment insurance to accommodate more frequent career transitions

- A serious political conversation about how productivity gains from automation are distributed across the economy

If financial restructuring is the primary driver, the more urgent conversation shifts to:

- Corporate governance and the misalignment between executive incentives and workforce stability

- The structural conditions under which companies can shed tens of thousands of workers while posting record revenues

- Whether current accountability mechanisms are adequate to the moment

Both dynamics are present simultaneously. The challenge is not choosing between these explanations but accurately apportioning the weight each deserves in specific cases. What is not analytically acceptable is allowing the AI narrative to absorb the full explanatory burden when a large share of the workforce disruption being experienced right now has roots in decisions made years before any meaningful AI deployment occurred.

What the Near-Term Outlook Actually Looks Like

The employment environment in the technology sector is unlikely to improve substantially in the near term, and the structural forces driving that outlook are more varied and entrenched than any single factor can account for.

Enterprise software companies that have completed major restructuring rounds are not likely to reverse course or rehire at historical rates, regardless of revenue performance. The cost efficiencies they have achieved are now built into margin expectations, and restoring them would require justifications that the current environment does not readily supply.

AI infrastructure investment is generating meaningful job creation at the companies building foundational models and the systems that support them, including Nvidia, Anthropic, OpenAI, and the major cloud providers. But those positions demand highly specialized skills and exist in numbers categorically smaller than the roles being eliminated across the broader industry.

The mid-market software problem

The mid-market software sector faces a particularly acute strategic challenge. The AI capabilities being embedded into the core platforms of Microsoft, Google, and Salesforce are encroaching directly on functionality that thousands of specialized SaaS companies have built their business models around.

That competitive displacement is driving restructuring decisions entirely independent of macroeconomic conditions, because the threat to those companies' product differentiation is structural and ongoing rather than cyclical.

What this means for individual workers

For professionals navigating this environment, the period ahead disproportionately rewards demonstrated adaptability and the capacity to deploy AI tools effectively as productivity multipliers within one's domain of expertise. The workers who are best positioned share a common profile:

- They have integrated AI capabilities into their existing domain fluency, not replaced it

- They exercise judgment in ambiguous, high-stakes situations that AI systems handle inconsistently

- They operate across functions, rather than as narrow specialists in roles that are themselves being automated

- They understand how to evaluate AI output critically, rather than treating it as a finished product

Narrow specialization in tool categories that are themselves being automated carries the highest career risk, while the ability to exercise nuanced judgment in complex or ambiguous situations remains, for now, a durable source of professional value.

Conclusion

Thirty thousand jobs eliminated in sixty days is a number with real human weight behind it, and the people affected deserve an honest accounting of the forces actually responsible, rather than a narrative crafted primarily for investor relations purposes.

The factual picture that emerges from careful analysis is this:

- AI is genuinely contributing to workforce restructuring in specific, well-documented domains, particularly customer support operations, certain software engineering support functions, and content production. Its impact in those areas is real, measurable, and accelerating.

- A substantial portion of the cuts across the broader technology sector reflect financial correction, overhiring remediation, and structural pressure to deliver operating margins that the growth-at-all-costs era never required companies to demonstrate.

- AI is being invoked to frame many of those decisions as transformation rather than retrenchment, and that conflation is doing meaningful harm to public understanding of what is actually happening.

The technology will continue to develop, and its impact on the composition of knowledge work will deepen and broaden over the coming years. But the narrative in which AI alone bears primary responsibility for the disruption being experienced across the tech workforce is simultaneously too convenient for the companies offering it and too incomplete for the workers and policymakers who need to make decisions grounded in an accurate understanding of the moment.

Both propositions can be true at once: AI is reshaping work in ways that are consequential and still accelerating, and the current layoff wave is, in substantial measure, about something else entirely.

Frequently Asked Questions

Q: Is AI directly responsible for the 2025 tech layoffs?

AI is a genuine contributing factor in specific job categories, particularly customer support, content production, and software testing. However, a significant portion of current layoffs reflects financial restructuring, overhiring corrections, and sustained investor pressure on operating margins rather than direct AI displacement. A number of companies are using AI investment as a narrative frame for reductions that are primarily cost-driven and rooted in organizational decisions made years before any meaningful AI deployment.

Q: Which tech jobs are most at risk from AI automation?

Roles characterized by high task repetition, clear output metrics, and limited requirements for contextual judgment face the most significant near-term exposure. This includes tier-one customer support, data entry and processing, templated content writing, basic financial reconciliation, and certain software QA functions. Roles that depend on strategic judgment, complex relationship management, physical presence, or creative synthesis remain more insulated, though no category should be considered permanently immune as the technology continues to develop.

Q: How many tech jobs have been lost to AI so far?

Isolating AI-attributable displacement from broader workforce reductions is methodologically difficult, as companies rarely specify AI as the direct cause of individual role eliminations. Goldman Sachs estimates that generative AI could automate 25 to 30 percent of work tasks across the U.S. economy over the next decade, but current displacement remains concentrated in specific functions and sectors rather than distributed broadly, and much of it manifests as reduced hiring rather than active terminations.

Q: Are tech companies being honest about why they're laying off workers?

Analysts and independent researchers have documented a pattern in which companies announce AI investment strategies alongside headcount reductions, using AI as partial narrative cover for what are primarily financial restructuring decisions. While AI is genuinely reshaping certain roles, attributing layoffs primarily to AI frequently overstates the technology's current operational impact and understates the degree to which these decisions reflect the financial correction of pandemic-era overhiring.

Q: What should tech workers do to protect their careers from AI disruption?

Professionals who develop fluency with AI tools as productivity multipliers within their existing domain of expertise are demonstrably better positioned than those who either ignore or resist the technology. Adaptability, cross-functional capability, and the ability to exercise informed judgment in ambiguous, high-stakes situations are increasingly valued as routine task work faces growing automation pressure. Narrow specialization in tool categories that are themselves subject to automation carries the greatest career risk over a three-to-five-year horizon.

Q: Which companies have cited AI as a reason for layoffs in 2025?

Salesforce has been among the most direct and explicit, with CEO Marc Benioff publicly linking the capabilities of its Agentforce platform to internal workforce planning decisions. Microsoft, Google, and Workday have all restructured teams in ways that correlate closely with AI capability development and deployment, though the direct causal relationship is more often implied in strategic communications than explicitly stated in public disclosures.

Q: Will AI cause a broader employment crisis in the tech sector?

Research from MIT, Goldman Sachs, and Stanford's HAI Institute collectively suggests that AI will reshape job tasks progressively over the next decade rather than producing sudden, concentrated displacement in the near term. The more significant near-term risk may be workforce compression: AI tools extending per-worker productivity in ways that reduce the pace of new hiring rather than triggering mass terminations, a mechanism that would have a substantial but less visible effect on employment levels and wage dynamics over time.

Related Articles