For decades, digital payments operated on a fixed assumption: a human being must actively confirm every transaction. On December 18, 2025, Visa announced that hundreds of secure purchases had been initiated, authenticated, and completed entirely by artificial intelligence agents, with no human pressing a button at checkout. These were not lab simulations but real purchases carried out by AI systems acting on behalf of consumers at actual merchants.

Rubail Birwadker, Visa's SVP and Head of Growth Products and Partnerships, framed the moment directly: "This holiday season marks the end of an era. In 2026, AI agents won't just assist your shopping. They will complete your purchases." Coming from a senior executive at one of the world's largest payment networks, that is a statement worth taking seriously.

What Visa Is Actually Building

The initiative sits under a platform Visa launched in 2025 called Visa Intelligent Commerce (VIC). The framework provides the infrastructure, APIs, tokenized payment credentials, authentication controls, and partner ecosystem that allow AI agents to make secure purchases on behalf of users.

The scale of the effort is already significant:

- More than 100 partners are working within the VIC ecosystem

- Over 30 are actively building within its sandbox environment

- More than 20 AI agents and agent enablers have integrated directly with the platform

- Hundreds of controlled, real-world agent-initiated transactions have been completed in live production settings as of December 2025

Visa also worked with AWS to make VIC available through the AWS Marketplace, allowing developers to embed agent payment capabilities directly into cloud-based workflows. The partnership released open-source blueprints within the Amazon Bedrock AgentCore repository covering retail shopping, travel booking, financial tasks, and post-purchase processes.

What the Early Pilots Look Like in Practice

The closed-beta partners give a clearer picture of how agentic commerce functions at the transaction level.

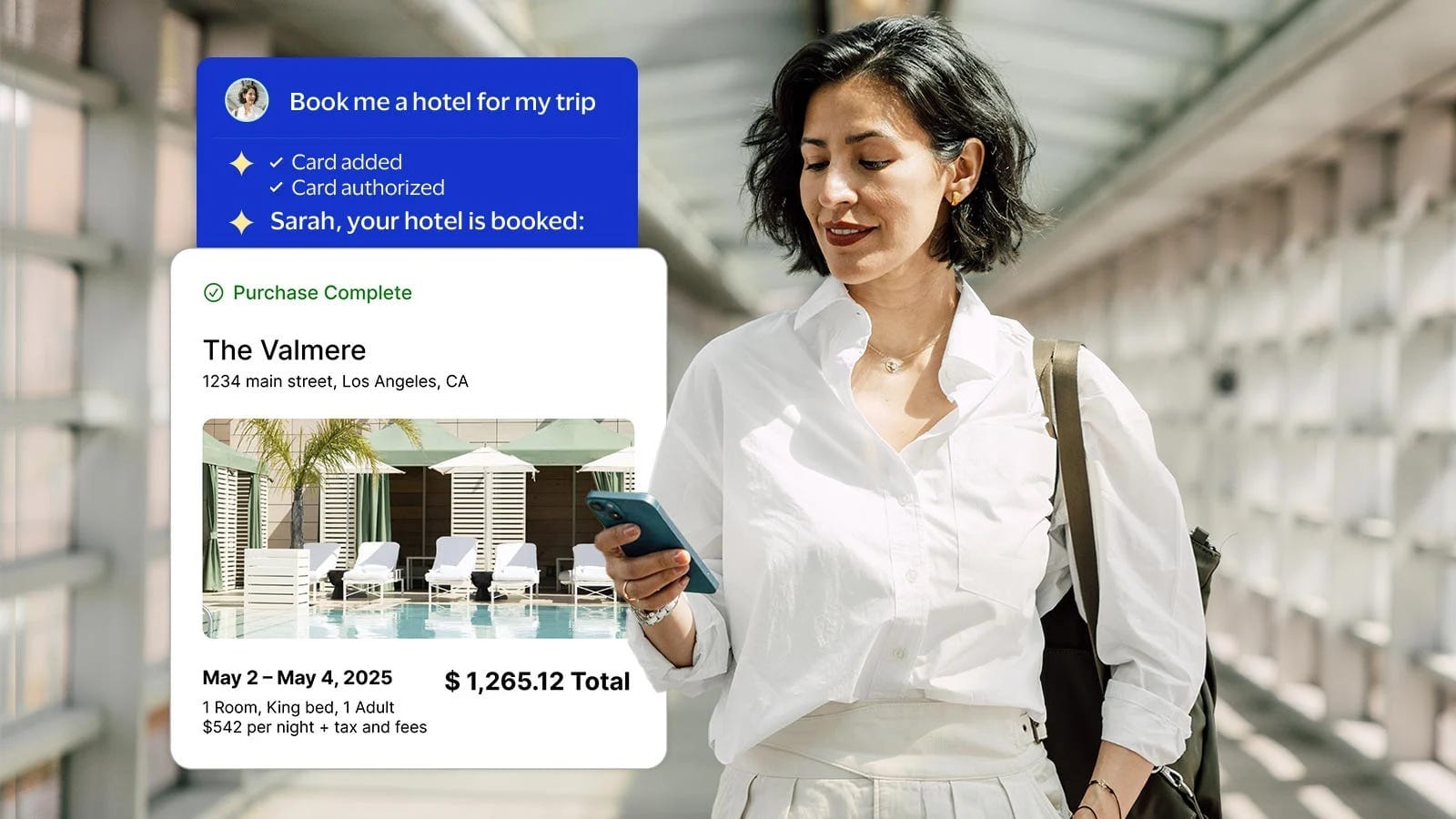

Skyfire enabled Consumer Reports' product recommendation agent to execute an actual purchase of Bose headphones through browser automation. The user set parameters; the agent found and bought the product without further input.

Nekuda built infrastructure that lets fashion app Gensmo take a user from AI-curated outfit recommendation to completed purchase at retailer Fabrique in a single tap, using Rye's checkout API. A separate Nekuda integration lets Price.com's AI shopping agent complete purchases at Honeylove via browser automation.

PayOS provided payment infrastructure for BeyondStyle, enabling agent-driven checkout at online retailer Jomashop. The user specifies preferences; the agent handles the rest.

Ramp applied VIC to its B2B automation platform to streamline corporate bill payments, allowing companies to automate routine spending while still capturing cashback on card transactions.

Each of these represents a different slice of the same underlying shift: the AI agent as a principal actor in the transaction, not a recommendation engine that stops before the buy button.

How the Technology Actually Works

The mechanics of agentic payments differ in a meaningful way from how digital payments work today. In a standard online transaction, the cardholder authenticates at the point of sale by entering details, using a saved card, or confirming through their bank's app, with authorization tied to that specific moment of human action.

In agentic commerce, authorization is separated from execution. The user sets permissions upstream, specifying which agents can spend, under what conditions, at which merchant categories, and up to what amounts. The agent then operates within those guardrails autonomously, completing transactions without further human confirmation. The payment credentials AI agents carry are tokenized rather than raw card numbers, using the same underlying technology Visa already uses for tap-to-pay and mobile wallets. Each token is scoped to specific usage rules and can be revoked by the cardholder at any time.

The Trusted Agent Protocol

The harder problem is merchant trust. Merchants already deal with massive volumes of automated traffic, much of it malicious bots probing for vulnerabilities, and when AI agents show up at checkout, merchants need a reliable way to distinguish a legitimate consumer-authorized agent from an unauthorized scraper or attacker.

In October 2025, Visa and more than 10 partners introduced the Trusted Agent Protocol (TAP), an open framework built on existing web infrastructure. Agents register their public keys in a Visa-managed directory before initiating transactions. When an agent makes a request, it cryptographically signs the HTTP message using its private key, and merchants and Visa can then verify that signature against the registered public key to confirm that a specific authorized agent is acting on behalf of a specific cardholder.

Akamai joined the initiative, integrating its edge-based behavioral intelligence and bot protection capabilities to strengthen identity verification and fraud controls at the merchant storefront. The TAP launch partners included Adyen, Ant International, Checkout.com, Coinbase, CyberSource, Elavon, Fiserv, Microsoft, Nuvei, Shopify, Stripe, and Worldpay. The breadth of that list signals that this is being treated as foundational payments infrastructure, not a pilot feature.

Mastercard Is Building the Same Thing

Visa is not moving alone. Mastercard has been building parallel infrastructure under its Agent Pay framework, also introduced in late 2025, centered on what it calls "agentic tokens": evolved versions of its existing tokenization technology designed specifically for agent-initiated transactions. The company completed its rollout to all U.S. issuers in November 2025 and is planning global expansion in early 2026. In September 2025, PayOS demonstrated the first live transaction using a Mastercard Agentic Token in a controlled proof-of-concept setting.

Both companies are converging on the same architecture: tokenized credentials, delegated authorization, and an identity layer that makes agents verifiable to merchants. When the two dominant global payment networks commit resources to the same infrastructure category simultaneously, it signals a bet on a behavioral shift, not just a feature roadmap.

The Startup Ecosystem Building Around It

A new category of infrastructure company has formed around agentic payments, and early funding patterns reflect the commercial opportunity. Basis Theory, Nekuda, and Skyfire have collectively raised nearly $50 million to build the financial rails for agent transactions. Nekuda raised a $5 million seed round from Madrona, Amex Ventures, and Visa Ventures. Skyfire raised $9.5 million from Neuberger Berman, a16z CSX, and Coinbase Ventures.

In December 2025, Stripe launched the Agentic Commerce Suite, a turnkey solution rolling out through Wix, WooCommerce, BigCommerce, Squarespace, and others. Early merchant adopters included URBN (Anthropologie, Free People, Urban Outfitters), Etsy, Coach, Kate Spade, Ashley Furniture, and Revolve. OpenAI announced a partnership with PayPal to bring commerce functionality directly into ChatGPT, and Salesforce and Stripe have integrated the Agentic Commerce Protocol to enable transactions initiated through AI agents.

Edgar, Dunn and Co. projects the agentic commerce total addressable market at $135 billion in 2025, growing to $1.7 trillion by 2030.

What the Consumer Behavior Data Shows

Visa commissioned research with Morning Consult in October 2025, covering 1,000 adults across 12 markets: the U.S., Canada, Mexico, Brazil, France, Germany, Spain, the U.K., Australia, the UAE, Singapore, and South Africa. Two findings stand out: 47 percent of U.S. shoppers now use AI tools for at least one part of the shopping journey, and Salesforce research found that 48 percent of consumers who currently use AI for shopping said they would allow an AI agent to complete a purchase on their behalf.

Both numbers suggest that the behavioral precondition for agentic commerce is already forming, even before the infrastructure is widely deployed. Adobe Analytics also reported a 1,200 percent jump in traffic from generative AI sources to retail websites in early 2025, meaning AI is already the browsing interface for a growing share of visitors, and the commercial extension of that is letting them buy.

The Real Risks Nobody Is Downplaying

Every participant in this ecosystem acknowledges that agentic commerce introduces risks that existing payment infrastructure was not designed to handle.

- Liability when agents make errors. Traditional payment disputes involve four parties: the consumer, the issuing bank, the acquiring bank, and the merchant. Agentic commerce introduces the AI platform as a fifth participant. When an agent books the wrong flight date, orders the wrong size, or misinterprets user intent, current frameworks do not clearly define who is responsible. Visa's Ramachandran has been explicit: "You must anticipate errors will occur and establish safeguards around that," and the frameworks to do so do not yet fully exist.

- Fraud and identity abuse. Visa has published a report outlining the risks of agent-driven transactions, including fraud, identity abuse, and unauthorized purchases. The Trusted Agent Protocol and tokenization are intended as safeguards, but they require merchant adoption and proper implementation to function as designed.

- Revocation and control. Consumers can revoke agent permissions, adjust spending limits, or require manual approval for purchases above specified thresholds. How well these controls are communicated and how easily they can be exercised in practice will determine whether consumers actually trust the system.

- The bot problem at scale. The same verification infrastructure designed to authenticate legitimate agents must also keep pace with sophisticated adversarial actors. As agentic commerce grows, the commercial incentive to compromise or impersonate authorized agents will grow alongside it.

Why the Payment Networks Are Moving Now

The timing of Visa and Mastercard's simultaneous push into agentic infrastructure reflects a specific strategic calculation. The payment networks control the rails through which money moves, and as AI agents become the primary interface through which consumers discover and purchase products, whoever controls the payment credentials and authorization protocols for those agents controls a new and consequential layer of the commerce stack.

OpenAI, Anthropic, Google, and Microsoft are all building AI systems with commerce intent, and those systems will need to execute payments. Visa and Mastercard are positioning themselves to be the trusted layer through which agent-initiated purchases are authenticated, authorized, and settled. If they establish that position, they extend their existing dominance into the agentic era. If they do not, alternative payment rails built around AI-native architectures could emerge to fill the gap, which is precisely why both networks are moving with unusual urgency.

Conclusion

Agentic commerce is moving from theoretical to operational faster than most of the payments industry anticipated. Visa has completed hundreds of real transactions in live environments, Mastercard has deployed its agentic token framework to all U.S. issuers, and a startup ecosystem measuring its addressable market in trillions has formed around the infrastructure required to make it work.

The shift is not simply about convenience. It is about where the authorization to spend sits in a transaction. Moving that authorization upstream, from the moment of purchase to a set of pre-configured permissions, changes the fundamental relationship between a consumer, their money, and the systems that move it. Visa predicts millions of consumers will use AI agents to complete purchases by the 2026 holiday season, and whether that number proves accurate, the structural direction it signals is already visible in the infrastructure being built around it.

Frequently Asked Questions

What is agentic commerce and how is it different from normal online payments?

Agentic commerce refers to transactions where an AI agent completes a purchase on behalf of a user, without the user manually entering payment details or confirming each transaction. The user sets permissions and spending rules in advance, and the agent operates autonomously within those parameters. Regular digital payments require a human to actively confirm each transaction at the point of sale, whereas agentic commerce moves that confirmation upstream and delegates execution to software.

What has Visa actually completed so far?

As of December 2025, Visa reported that hundreds of secure, agent-initiated transactions had been completed in real-world, live production environments with partners including Skyfire, Nekuda, PayOS, and Ramp. Actual purchases were made at actual merchants, with AI agents handling authentication, authorization, and payment execution without human involvement at checkout.

How does Visa's Trusted Agent Protocol work?

The Trusted Agent Protocol is an open verification framework in which AI agents register their public keys in a Visa-managed directory before initiating transactions. When an agent makes a purchase request, it cryptographically signs the HTTP message with its private key, and merchants and Visa verify that signature against the registered public key to confirm the agent is authorized to act on behalf of a specific cardholder. This allows merchants to distinguish legitimate consumer-authorized agents from malicious bots.

Is Mastercard also building agentic payment infrastructure?

Yes. Mastercard launched its Agent Pay framework in late 2025, using "agentic tokens" evolved from its existing tokenization technology. The company completed its rollout to all U.S. issuers in November 2025 and is planning pilots in Europe and Asia Pacific in early 2026.

Can consumers control what AI agents are allowed to buy?

Yes. The model requires consumers to set spending rules and permissions before the agent can act. Users can specify which agent systems are authorized, at which merchant categories, up to what spending limits, and whether high-value transactions require manual approval. Users can also revoke agent access at any time, though how easily those controls are implemented in practice is one of the open questions around consumer adoption.

What happens when an AI agent makes a purchasing error?

Current payment dispute frameworks are designed for transactions with four parties: consumer, issuing bank, acquiring bank, and merchant. Agentic commerce introduces the AI platform as a fifth participant, and the question of who bears liability when an agent books incorrectly, purchases the wrong item, or misinterprets instructions has not been clearly defined by industry frameworks yet. Payment executives have acknowledged this as a genuine unresolved problem.

How large is the agentic commerce market expected to become?

Edgar, Dunn and Co. projects the agentic commerce total addressable market at $135 billion in 2025, growing to $1.7 trillion by 2030, representing a compound annual growth rate of approximately 67 percent. Visa predicts millions of consumers will use AI agents to complete purchases by the 2026 holiday season.

What other companies besides Visa and Mastercard are building agentic commerce infrastructure?

Stripe launched its Agentic Commerce Suite in December 2025, rolling out through Wix, WooCommerce, BigCommerce, Squarespace, and others. OpenAI has partnered with PayPal to bring commerce functionality into ChatGPT. Salesforce and Stripe have integrated the Agentic Commerce Protocol. Infrastructure startups including Nekuda, Skyfire, PayOS, and Ramp are building the payment rails and agent enablement tools within the Visa Intelligent Commerce ecosystem.

Related Articles