Every quarter, dozens of tech companies report earnings. Most of them tell you something about a product, a market, or a management team.

TSMC's earnings tell you something different. They tell you how much AI infrastructure the world is actually building, because nearly every advanced chip powering that infrastructure starts in a TSMC fabrication plant.

Today's Q1 2026 results are the most consequential data point the AI industry will see this quarter.

The Numbers

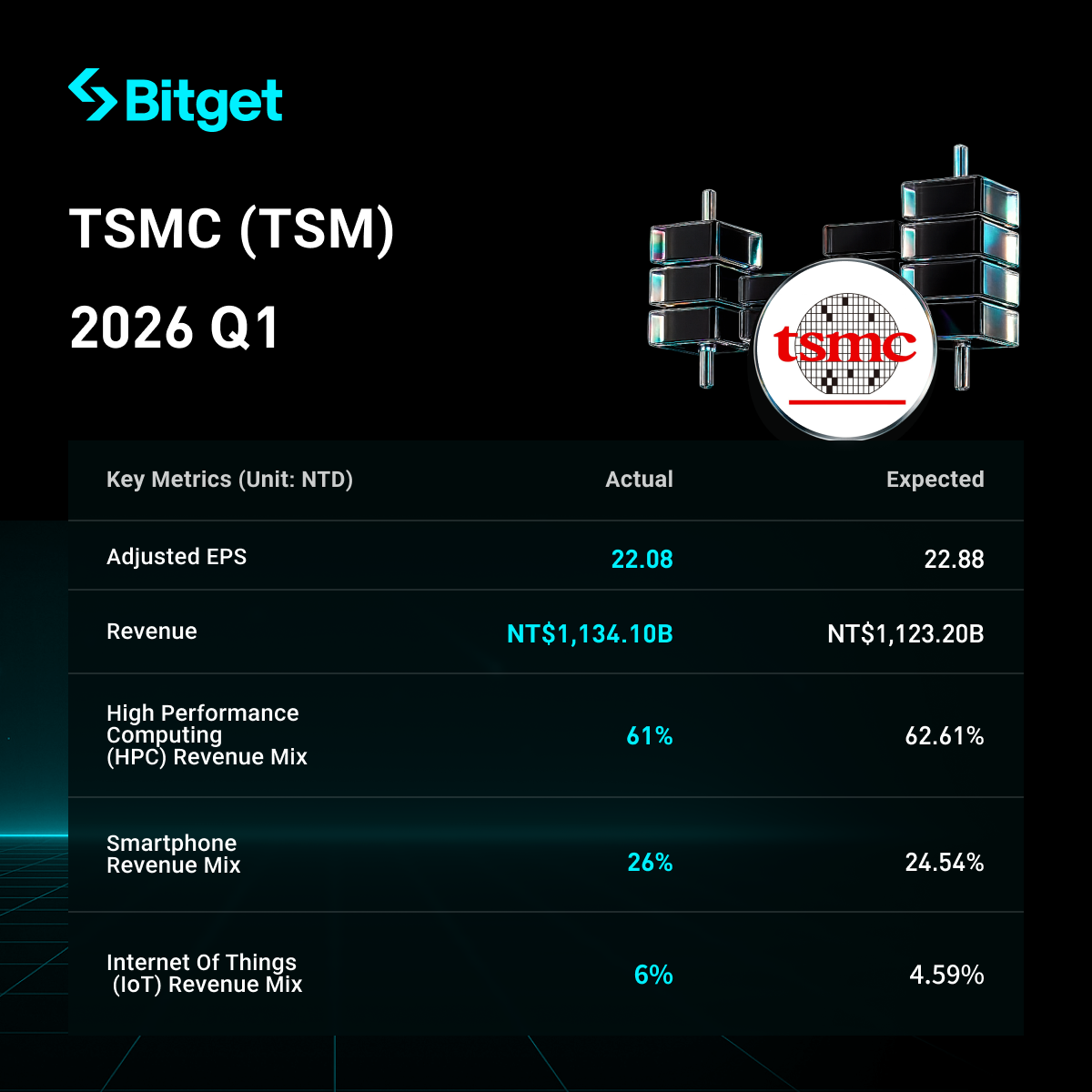

TSMC reported consolidated revenue of NT$1,134.10 billion for Q1 2026, or $35.90 billion in US dollar terms, up 40.6% year-over-year and up 6.4% from Q4 2025.

In Taiwan dollar terms, revenue grew 35.1% year-over-year, beating the analyst consensus of NT$1.12 trillion. It marks the first time TSMC has broken the NT$1 trillion quarterly revenue threshold.

Net income reached NT$572.48 billion, a 58.3% year-over-year increase. Diluted EPS came in at NT$22.08, beating the analyst consensus of NT$20.88 by a meaningful margin.

The margin profile was equally strong. Gross margin reached 66.2%, well above the guidance range of 63% to 65% and above the analyst consensus of 64.5%. Operating margin came in at 58.1%, and net profit margin at 50.5%.

March was the single biggest month of the quarter. Revenue for March alone hit NT$415.19 billion, up 45.2% year-over-year and the strongest monthly print in TSMC's history.

What CC Wei Said

TSMC Chairman and CEO CC Wei was direct on the earnings call.

"AI related demand continues to be extremely robust," he said. On the question of supply tightness, Wei's response left no ambiguity: advanced-node output is running at roughly one-third of what major customers expect to use. When asked why TSMC had revised its 2026 capital expenditure to the top of its $52 billion to $56 billion range, Wei's answer was characteristically brief: "The demand are very robust, especially from the HPC and AI applications. We try very hard to speed it up and pull in all the equipment as we can. Still, our supply is very tight."

Wei also characterized AI as "the multi-year AI megatrend" and raised the company's full-year revenue growth guidance from approximately 30% to above 30% in US dollar terms.

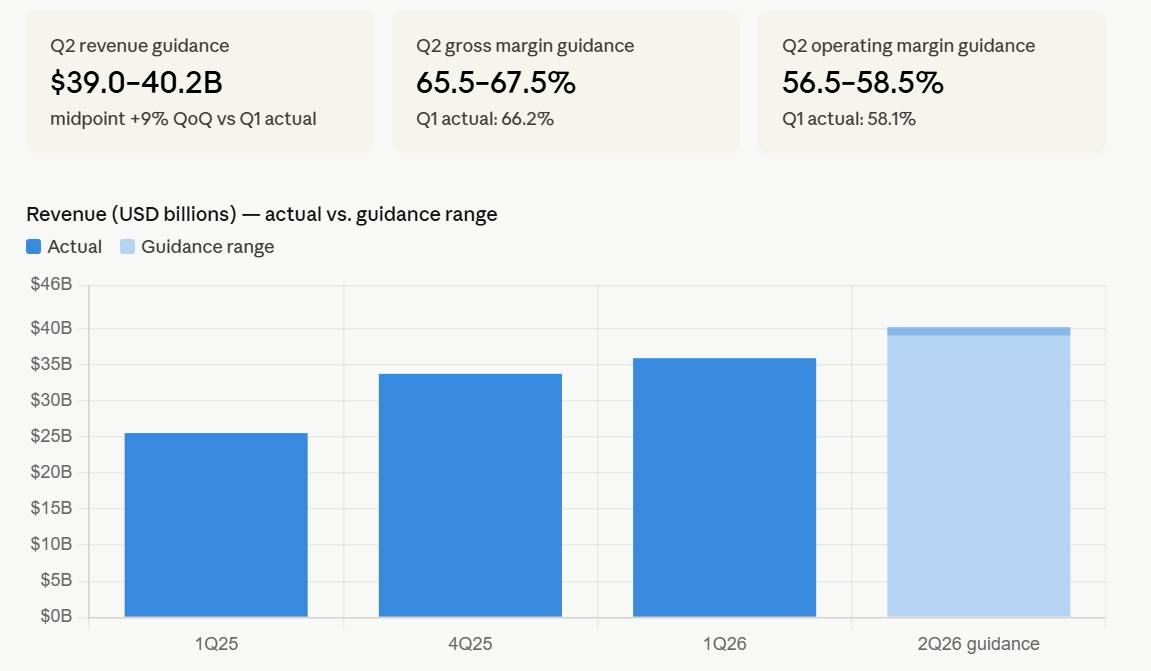

Q2 Guidance and What It Signals

TSMC guided Q2 2026 revenue of $39 billion to $40.2 billion.

Analysts had been expecting approximately $38.1 billion. The midpoint of TSMC's guidance is $39.6 billion, roughly $1.5 billion above consensus.

That gap matters. It means the AI infrastructure buildout is not just holding at current levels but is continuing to accelerate into Q2. It also implies full-year revenue growth is tracking significantly above the prior guidance of approximately 30%.

For context, Q2 2025 revenue was $30.1 billion. A Q2 2026 midpoint of $39.6 billion would represent roughly 31.5% year-over-year growth even at the guidance midpoint, and above 33% at the top end.

The Node Mix: Where the Growth Is Coming From

TSMC's revenue is not growing uniformly across process nodes. The concentration in leading-edge processes is significant and widening.

In Q1 2026, shipments of 3-nanometer chips accounted for 25% of total wafer revenue. That compares to just 6% of revenue in Q3 2023. The 5-nanometer node accounted for 36%, and 7-nanometer accounted for 13%. Advanced technologies at 7nm and below collectively represented 74% of total wafer revenue in the quarter.

The 3nm expansion is directly tied to AI accelerator demand. Nvidia's current-generation GPUs, Apple's custom silicon, AMD's data center GPUs, and the hyperscalers' custom ASICs all run on advanced TSMC nodes, and most of the incremental volume is going to AI workloads rather than consumer devices.

Smartphone and PC end markets actually took a hit in Q1 2026 due to memory shortages. AI carried the entire semiconductor sector.

The 2nm Ramp and What It Means for Pricing Power

TSMC's 2nm process node entered volume production in Q4 2025 at its Hsinchu and Kaohsiung facilities, ahead of the original schedule, with initial yields reportedly exceeding internal expectations.

The 2nm node family, which includes the base N2 process along with the enhanced N2P variant and the HPC-optimized A16 node, is shaping up to be one of the most consequential process generations in TSMC's history. The A16 architecture introduces a new power delivery system specifically designed for the high power density requirements of AI and data center computing.

Wafer prices for 2nm are expected to exceed $30,000 per wafer, compared to approximately $20,000 for 3nm. SemiAnalysis analyst Sravan Kundojjala described TSMC's price increases for advanced nodes as a "big factor" in the revenue outperformance this quarter.

The pricing dynamic is structural rather than opportunistic. When demand runs at three times available supply and lead times exceed 50 weeks, pricing power is simply a function of supply and demand.

The CoWoS Bottleneck That Most Coverage Misses

Advanced chip fabrication gets most of the attention in TSMC coverage. Advanced packaging is the constraint that is actually gating AI hardware shipments right now.

CoWoS, which stands for Chip-on-Wafer-on-Substrate, is the 2.5D packaging technology that stacks high-bandwidth memory alongside AI accelerators. Without CoWoS capacity, even a completed wafer cannot be assembled into a finished AI chip. Nvidia has reportedly reserved more than 50% of TSMC's CoWoS packaging capacity for 2026 and 2027.

TSMC is scaling CoWoS capacity aggressively, targeting a doubling from approximately 35,000 wafers per month in 2024 to 70,000 by end-2025 and further expansion through 2026. Approximately 10% to 20% of the 2026 capex budget is allocated to advanced packaging and test facilities specifically.

Two dedicated packaging plants in Arizona are part of TSMC's US expansion plan, in addition to the wafer fabrication facilities.

Capex at the Top of the Range: What It Means for the Supply Chain

TSMC revised its 2026 capital expenditure guidance to the top of the $52 billion to $56 billion range.

That is roughly a 37% increase over the $40.9 billion spent in 2025, and it is the single most consequential number in the entire semiconductor supply chain. Every dollar of TSMC capex flows through to equipment suppliers.

ASML, which makes the extreme ultraviolet lithography machines required for 3nm and 2nm production, reported Q1 2026 gross margin of 53%. Applied Materials, Lam Research, and KLA all have direct revenue exposure to TSMC's leading-edge ramp. When TSMC confirms it is spending toward the top of its capex range, those companies' revenue pipelines are effectively confirmed for the next 18 to 24 months.

The Arizona buildout has total commitments of up to $165 billion, with plans for as many as 12 fabrication plants, funded partly through the US CHIPS Act. Progress on the Fab 21 3nm facility and timeline for 2nm production at the US site were on the agenda for today's call.

The Geopolitical Dimension

TSMC controls approximately 70% of the global advanced chip foundry market. Every major AI accelerator running in every major data center globally depends on TSMC's manufacturing capacity.

That concentration, combined with Taiwan's geographic position relative to mainland China, has driven one of the most significant industrial diversification efforts in modern history. The Arizona buildout, the Japan facilities in Kumamoto, and the planned European presence are all expressions of the same strategic reality: customers and governments cannot accept a world in which the entire AI computing supply chain runs through one island.

Wei acknowledged global tariff policies as a risk factor for 2026 on the call. Overseas production in Arizona, Japan, and Germany operates at lower margins than TSMC's Taiwan facilities, where the most advanced work is concentrated. The geographic diversification reduces political risk at the cost of margin efficiency.

The Iran war that began in late February 2026 was another variable markets were watching going into this quarter. Supply chain analysts were tracking potential impacts on helium and specialty gas supply chains, both of which are inputs to semiconductor manufacturing. March's 45.2% year-over-year growth confirms those concerns did not materialize into demand disruption.

Why This Report Matters Beyond TSMC

TSMC's revenue is a direct measurement of AI infrastructure investment, stripped of the hype that surrounds model announcements, product launches, and corporate AI strategy presentations.

When hyperscalers report AI investment intentions, those intentions can be revised. When AI labs announce compute plans, those plans can shift. When TSMC reports revenue and raises guidance, it is reporting what has already been manufactured and what customers have already committed to build next.

The Q1 2026 numbers confirm three things that matter for the broader market.

First, AI infrastructure investment is not decelerating. The year-over-year growth rate accelerated from Q4 2025 to Q1 2026, and the Q2 guidance puts the trajectory above consensus.

Second, the physical constraints are real and binding. TSMC's supply is at roughly one-third of demand at the leading edge, lead times exceed 50 weeks, and packaging capacity is fully committed through 2027. That is a supply picture, not a demand question.

Third, the pricing power flowing from those constraints is shifting the semiconductor industry's margin structure. A gross margin of 66.2% at a company of TSMC's scale is a signal about where value is concentrating in the AI supply chain.

Conclusion

TSMC's Q1 2026 results are not primarily a story about one company.

They are a measurement of how much the world is spending to build the physical infrastructure that AI runs on, reported by the company that fabricates roughly nine of every ten advanced AI chips on the planet.

Revenue of $35.9 billion, net income up 58%, gross margins of 66.2%, Q2 guidance $1.5 billion above consensus, capex revised to the top of the range, and CC Wei calling AI demand "extremely robust" on every relevant dimension.

The AI buildout is not slowing. The numbers say so directly.

Frequently Asked Questions

What were TSMC's Q1 2026 earnings results?

TSMC reported Q1 2026 revenue of $35.90 billion, up 40.6% year-over-year in US dollar terms and up 35.1% in Taiwan dollar terms. Net income was NT$572.48 billion, a 58.3% year-over-year increase. Gross margin was 66.2%, above guidance of 63% to 65%. Diluted EPS of NT$22.08 beat the analyst consensus of NT$20.88.

What did TSMC guide for Q2 2026?

TSMC guided Q2 2026 revenue of $39 billion to $40.2 billion, with analyst consensus at approximately $38.1 billion prior to the report. The guidance implies continued acceleration into Q2. TSMC also raised its full-year 2026 revenue growth guidance from approximately 30% to above 30% in US dollar terms.

Why is TSMC's earnings report important for the AI market?

TSMC fabricates approximately 70% of the world's advanced chips, including virtually all major AI accelerators from Nvidia, AMD, Apple, and hyperscaler ASICs. Its revenue is a direct measurement of actual AI infrastructure spending rather than stated investment intentions. When TSMC grows revenue 35% and raises guidance, it confirms the physical AI buildout is continuing to accelerate.

What is TSMC's capex plan for 2026?

TSMC revised its 2026 capital expenditure to the top of its $52 billion to $56 billion guidance range, up approximately 37% from the $40.9 billion spent in 2025. CEO CC Wei attributed the revision to "extremely robust" demand that continues to outpace supply. TSMC separately has committed up to $165 billion for US manufacturing expansion, including up to 12 fabrication plants in Arizona.

What process nodes are driving TSMC's growth?

In Q1 2026, the 3-nanometer node accounted for 25% of total wafer revenue, up from 6% in Q3 2023. The 5-nanometer node accounted for 36%. Advanced technologies at 7nm and below represented 74% of total wafer revenue. The 2-nanometer node entered volume production in Q4 2025 ahead of schedule, with wafer prices expected to exceed $30,000 per wafer.

Related Articles