In late 2022, OpenAI had no meaningful revenue. By February 2026, it crossed $25 billion in annualized run rate, a milestone it reached in roughly 39 months. Salesforce took about 18 years to reach $25 billion in annual revenue. Google took about 17. Facebook took about 12. No software company in history has scaled to this revenue level this quickly.

That growth is genuinely impressive. What follows it, including the losses, the cash burn trajectory, the IPO preparations, and the structural tension between the company's founding mission and its commercial reality, is where the more important analysis lives.

The Revenue Picture: What $25 Billion Actually Represents

OpenAI reached $25 billion in annualized revenue at the end of February 2026, up 17 percent from $21.4 billion at year-end 2025. Full-year 2025 revenue came in at $13.1 billion, beating the company's own forecast by roughly $100 million. The projections for 2026 and 2027 are $30 billion and $62 billion respectively.

| Revenue Stream | 2025 Estimated | 2030 Projected |

|---|---|---|

| Consumer subscriptions (Plus, Pro, Team) | Largest driver | $150 billion |

| Enterprise and ChatGPT Enterprise | $2 billion | $70 billion |

| Developer API | Growing | $47.5 billion |

| Advertising and hardware | Near zero | $15 billion |

The consumer subscription business remains the primary engine. ChatGPT Plus at $20 per month accounts for roughly 15 million active subscribers, with higher tiers at $200 per month for Pro users and $25 to $30 per seat for small business teams. Enterprise seats list at approximately $60 per month. More than 9 million paying business users were on the platform as of February 2026, up from 5 million in August 2025, and weekly active users across all tiers reached 910 million.

The advertising direction is one of the more significant and underreported strategic shifts in OpenAI's history. Sam Altman called advertising a "last resort" as recently as May 2024, but by January 2026 the company was running targeted ads in ChatGPT for users on free and Go tiers. Internal projections show $1 billion in ad revenue for 2026, scaling to $25 billion by 2029. Anthropic took the opposite position entirely, running a Super Bowl ad that explicitly committed Claude to remaining ad-free.

The Cost Structure: Why Revenue Growth Has Not Solved the Problem

OpenAI projects cash burn of $25 billion in 2026 alone, rising to $57 billion in 2027. In 2025, the company generated $13.1 billion in revenue and spent approximately $22 billion to do it, spending roughly $1.69 for every dollar earned. Gross margins fell from 40 percent in 2024 to 33 percent in 2025, well below the company's own 46 percent target.

The central cost problem is inference, meaning the day-to-day expense of running AI models when users submit queries. Inference costs quadrupled in 2025 as demand for ChatGPT and API services outpaced available compute capacity, forcing OpenAI to purchase computing resources at emergency prices. Every additional user makes the company incrementally more expensive to operate rather than incrementally more profitable at current margin levels.

| Year | Revenue | Cash Burn | Gross Margin |

|---|---|---|---|

| 2024 | $6 billion | Moderate | 40% |

| 2025 | $13.1 billion | $8 to $9 billion | 33% |

| 2026 (projected) | $30 billion | $25 billion | Recovering |

| 2027 (projected) | $62 billion | $57 billion | 52 to 67% |

| 2030 (projected) | $200 to $280 billion | Turns positive | Above 50% |

Internal projections, reported by the Wall Street Journal and The Information, show cumulative cash burn of approximately $665 billion through 2030, revised upward by $111 billion from estimates made just two quarters earlier. The company's largest single-year operating loss is projected at approximately $74 billion in 2028, before turning cash-flow positive sometime in 2029 or 2030. HSBC analysts, offering an independent assessment, projected a remaining funding shortfall of approximately $207 billion beyond what is already raised or committed, and suggested profitability may arrive later than OpenAI's own projections indicate.

OpenAI CFO Sarah Friar has argued that the company has healthy underlying margins and could break even if it chose to, framing the spending as a deliberate strategic investment rather than an economic constraint. The analogy invoked most frequently is Amazon, which ran deeply negative cash flows while building AWS and rewarded patient investors with extraordinary long-term returns. The central question for public market investors will be whether OpenAI's infrastructure spending produces similarly durable competitive advantages, or whether the compute it is purchasing depreciates rapidly as model costs fall and competitors close the capability gap.

The Competitive Picture: Anthropic Is Closing Faster Than Expected

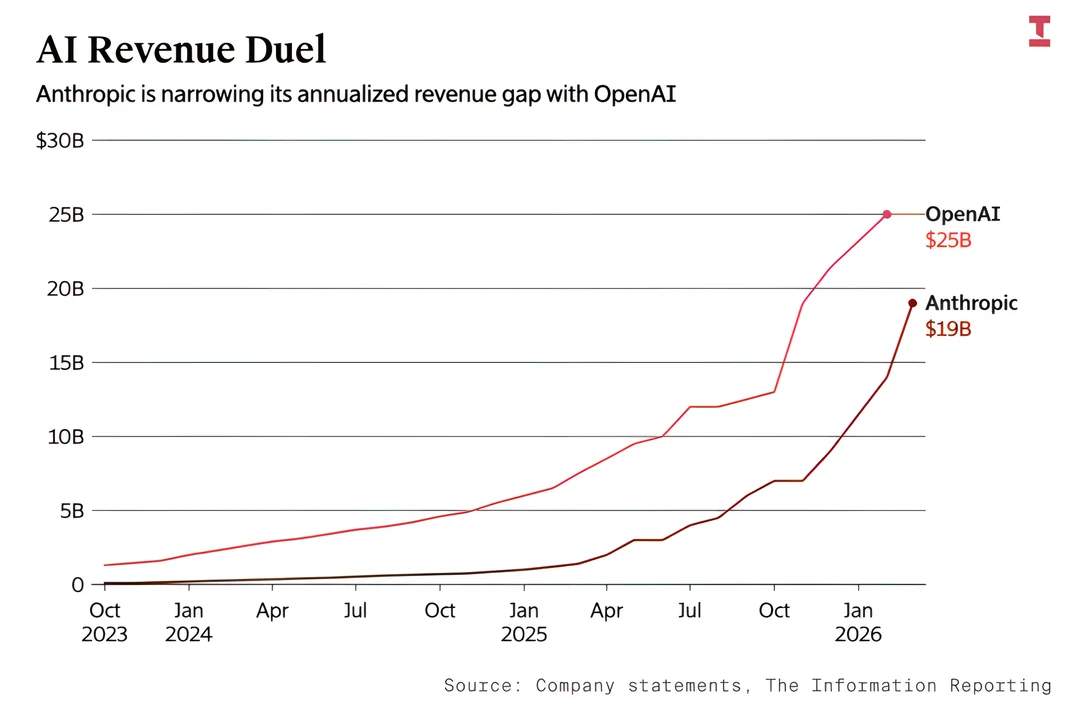

OpenAI's $25 billion revenue lead would be more comfortable if the distance between it and its nearest competitor were widening. Based on current trajectories, it is not.

Anthropic reached approximately $19 billion in annualized revenue as of early March 2026, representing a nearly tenfold increase over the prior year. Claude Code alone generated $2.5 billion in annualized revenue, more than doubling since the start of 2026. Epoch AI has projected that if both companies maintain current growth trajectories, Anthropic could overtake OpenAI in annualized revenue sometime between 2026 and 2027, at a convergence point of approximately $43 billion for both.

| Dimension | OpenAI | Anthropic |

|---|---|---|

| Annualized revenue (early 2026) | $25 billion | $19 billion |

| 2025 gross margin | 33% | Higher and improving |

| Cash burn rate (2026) | 57% of revenue | Declining toward 33% |

| Break-even target | 2030 | 2028 |

| Valuation (latest round) | $730 billion | $380 billion |

| Revenue mix | Consumer-heavy | 80% enterprise |

| Strategy | Broad platform, advertising | Focused enterprise, no advertising |

Anthropic's enterprise concentration produces a more predictable, higher-margin revenue profile and a meaningfully faster path to break-even. The company is deliberately avoiding OpenAI's costly expansions into image and video generation, robotics research, and consumer hardware, focusing instead on building the most reliable model for enterprise coding, analysis, and document workflows.

For investors evaluating both companies, the two-year gap in profitability timelines is not abstract. Investors in a company closer to break-even face substantially less dilution risk across multiple fundraising rounds, which gives Anthropic a structural advantage in its next phase of capital raising that compounds regardless of the current revenue differential.

The IPO: Structure, Valuation, and What It Would Accomplish

OpenAI completed the organizational restructuring that makes a public offering possible in October 2025, converting from a nonprofit-controlled capped-profit entity into a public benefit corporation called OpenAI Group PBC. The nonprofit arm, now called the OpenAI Foundation, retains a 26 percent equity stake in the company and a warrant to receive additional shares if certain milestones are met. Microsoft holds approximately 27 percent of the for-profit entity, a position valued at roughly $135 billion.

Law firms Cooley and Wachtell Lipton Rosen and Katz have been engaged to lead IPO preparations. Standard pre-IPO hires have been made, including a Chief Accounting Officer and Head of Investor Relations. CFO Sarah Friar has told associates the company is targeting a 2027 listing, while some advisers believe a regulatory filing could come as early as the second half of 2026.

On the valuation: OpenAI raised $110 billion in February 2026 at a pre-money valuation of approximately $730 billion. Internal projections and reporting from Reuters and Bloomberg suggest the company is targeting up to $1 trillion at IPO, which would be the largest public offering in history, surpassing Saudi Aramco's $25.6 billion raise in 2019 and Alibaba's $26 billion in 2014.

At $1 trillion, the implied multiples are approximately 38 times projected 2026 revenue, 5 times projected 2030 revenue, and 17 to 18 times projected 2030 operating income at a 10 to 20 percent margin. Those multiples are aggressive by conventional software metrics and potentially defensible for a company growing at triple-digit rates in a winner-take-most market, provided revenue projections materialize and margins recover as predicted.

What would make the valuation credible: revenue reaching $62 billion in 2027, gross margins recovering toward 52 to 67 percent from the current 33 percent, enterprise revenue scaling from $2 billion in 2025 to $70 billion by 2030, and advertising proving viable at the scale the company is projecting.

What would make the valuation vulnerable: continued gross margin compression, Anthropic or Google closing the model capability gap materially, revenue growth decelerating below projected trajectories, or public market investors applying software-company margin expectations to what is fundamentally an infrastructure-intensive business.

On the capital imperative: HSBC's $207 billion funding shortfall projection illustrates why private markets, even at OpenAI's fundraising velocity, cannot sustainably bridge the gap indefinitely. A further structural incentive exists through Amazon's $50 billion investment commitment, of which only $15 billion is upfront. The remaining $35 billion is contingent on OpenAI either achieving artificial general intelligence or completing an IPO, a contractual structure that directly accelerates the public market timeline regardless of the company's internal preferences.

What This Means for Users, Enterprise Buyers, and the Broader Market

For ChatGPT users, the most direct implications involve advertising and pricing. Ads began appearing for free and Go tier users in January 2026, with projections showing ad revenue scaling from $1 billion in 2026 to $25 billion by 2029. Premium subscription tiers will likely expand as public market pressure to demonstrate profitability intensifies. The countervailing force for users is competition: the intensity of rivalry among OpenAI, Anthropic, Google, and Meta has kept capability improvements rapid and per-unit pricing relatively stable, and whether that dynamic persists post-IPO is one of the more consequential questions in AI consumer markets.

For enterprise buyers, the IPO preparation is a signal worth taking seriously when evaluating vendor concentration risk. A company under public market scrutiny faces pressure to prioritize margin expansion and revenue growth in ways that private companies can defer indefinitely. That pressure typically manifests as price increases, tier restructuring, and reduced tolerance for custom arrangements that do not scale. The key due diligence question is not which model is currently best, since that assessment changes frequently, but whether OpenAI's financial structure makes it a durable long-term infrastructure partner. The 2028 versus 2030 profitability differential between Anthropic and OpenAI is a vendor risk consideration, not only an investor concern.

For the broader AI ecosystem, OpenAI's IPO will be the first major test of whether public markets can accurately price frontier AI infrastructure at scale. CoreWeave, which went public in early 2026 at a $23 billion valuation and roughly tripled from there, demonstrated that AI infrastructure companies can attract premium public market valuations. OpenAI will test whether that appetite extends to companies projecting $665 billion in cumulative cash burn before turning profitable. A successful offering at or near $1 trillion would validate high valuations across AI-adjacent companies and likely accelerate Anthropic's own public market preparations. A disappointed IPO would tighten capital availability for the AI startup ecosystem more broadly.

At its core, OpenAI's financial structure is an argument that frontier AI economics resemble infrastructure investment more than software investment: enormous upfront capital requirements, long payback periods, and eventually durable competitive advantages for the companies that survive the investment phase. The IPO is the mechanism through which that argument will be tested by a market with less patience and far more rigorous disclosure requirements than any private investor to date.

Frequently Asked Questions

How did OpenAI grow from near-zero to $25 billion in revenue so quickly?

OpenAI reached $25 billion in annualized revenue in approximately 39 months from near-zero in late 2022, driven by the rapid consumer adoption of ChatGPT and accelerating enterprise deployment. Revenue grew from $2 billion in 2023 to $6 billion in 2024 to $13.1 billion in 2025, with the annualized run rate reaching $25 billion by the end of February 2026. No software company in history has scaled to this revenue level in a comparable timeframe.

If OpenAI makes $25 billion, why is it still losing money?

Revenue and profitability are separate questions at OpenAI's current investment stage. The company generated $13.1 billion in revenue in 2025 and spent approximately $22 billion to do it, with gross margins falling to 33 percent as inference costs quadrupled due to demand outpacing compute capacity. The company projects cash burn of $25 billion in 2026 and $57 billion in 2027, with cumulative cash burn through 2030 projected at approximately $665 billion, and does not expect positive cash flow until 2029 or 2030.

What is the timeline for OpenAI's IPO?

CFO Sarah Friar has told associates the company is targeting a 2027 listing, while some advisers believe a late 2026 regulatory filing is possible. Law firms Cooley and Wachtell Lipton Rosen and Katz have been engaged, and standard pre-IPO hires have been made. The IPO was made structurally possible by the October 2025 conversion to a public benefit corporation. OpenAI's official stated position is that an IPO is not its current focus.

What valuation is OpenAI targeting for its IPO?

OpenAI is reportedly targeting a valuation of up to $1 trillion, which would be the largest public offering in history. Its most recent private round in February 2026 valued it at approximately $730 billion. At $1 trillion, the company would trade at roughly 38 times projected 2026 revenue of $30 billion, a multiple that is aggressive by conventional software standards but potentially defensible given the growth rate and platform position.

How does Anthropic compare to OpenAI financially?

Anthropic reached approximately $19 billion in annualized revenue as of early March 2026. Key strategic differences include generating approximately 80 percent of revenue from enterprise customers, targeting break-even by 2028 rather than OpenAI's 2030 target, and deliberately avoiding costly expansions into advertising, video generation, and consumer hardware. Epoch AI has projected Anthropic could overtake OpenAI in annualized revenue between 2026 and 2027 if both companies maintain current growth trajectories.

What does OpenAI's IPO mean for everyday ChatGPT users?

The most direct implications involve advertising and pricing evolution. Ads began appearing for free and Go tier users in January 2026, with internal projections showing advertising scaling from $1 billion in 2026 to $25 billion by 2029. Premium subscription tiers will likely expand under public market profitability pressure. Competitive pressure from Anthropic, Google, and Meta has so far kept capability improvements rapid and prices relatively stable, and whether that dynamic persists after the IPO is one of the more consequential open questions for AI consumers.

Why does OpenAI need an IPO when it keeps raising private capital?

HSBC projects OpenAI still faces a funding shortfall of approximately $207 billion beyond already-committed capital through 2030, which illustrates the limits of even the most active private fundraising program. Public markets provide access to deeper capital pools, the ability to make large acquisitions using public stock, and a liquidity mechanism for employees and early investors. Amazon's $50 billion investment commitment also includes a clause making $35 billion contingent on OpenAI either achieving AGI or completing an IPO, creating a direct contractual incentive to go public.

Related Articles