Two major research papers published in early 2026 have produced the most comprehensive picture yet of where AI is actually delivering productivity gains and where it is not. One surveyed nearly 6,000 executives across four countries. The second drew on almost 750 corporate CFOs.

The headline finding is not that AI is failing. Its benefits are arriving unevenly, concentrated at larger, more productive, better-paying firms, while smaller companies are still deciding whether the technology is worth the investment.

The first paper, "Firm Data on AI," is NBER Working Paper 34836 by Ivan Yotzov, Jose Maria Barrero, Nicholas Bloom, and collaborators across the US, UK, Germany, and Australia. The second, "Artificial Intelligence, Productivity, and the Workforce: Evidence from Corporate Executives," is NBER Working Paper 34984 by Salomé Baslandze and colleagues at the Federal Reserve Banks of Atlanta and Richmond and Duke University. Together, they provide a ground-level view of AI adoption that earnings call optimism does not.

The State of AI Adoption: Wide but Shallow

Across the US, UK, Germany, and Australia, 69 percent of businesses surveyed report currently using some form of AI technology. The most common uses are text generation using large language models, followed by visual content creation and data processing using machine learning.

The depth of that adoption tells a different story. Among senior executives, including CEOs and CFOs, more than two-thirds report using AI in a typical working week, but their average use is only 1.5 hours per week. A full quarter of senior executives report no AI use at all.

Country-level adoption rates across the four countries surveyed:

- United States: 78 percent of firms using AI

- United Kingdom: 71 percent

- Germany: 65 percent

- Australia: 59 percent

Across all four countries, 75 percent of firms expect to use AI within three years.

Who Is Actually Using AI

The research is specific about which firms are pulling ahead. Larger, more productive, and higher-paying firms are significantly more likely to be using AI. Younger firms with younger directors are also ahead of older firms. The pattern is consistent across all four countries surveyed.

The investment gap by firm size is stark. Around 30 percent of large firms expect to invest more than $1 million in AI in 2026. For smaller firms, the equivalent figure is 1 percent. Nearly 60 percent of smaller firms plan to invest less than $20,000 in AI over the same period, compared to 14 percent of larger firms.

This describes a bifurcated market where large firms are building infrastructure and smaller firms are still at the threshold of meaningful investment.

The Productivity Numbers: Positive but Modest

The CFO-focused paper finds that labor productivity gains from AI are real across sectors, though they vary significantly in magnitude. Firms in high-skill services, particularly finance, are seeing the largest gains, with implied annual labor productivity growth of approximately 0.8 percent. Firms in low-skill services, manufacturing, and construction see smaller but still positive gains of roughly 0.4 percent. These effects are expected to strengthen in 2026.

Among the CFO respondents, 40 percent reported no AI investment in 2025. Among those non-adopters, the reasons break down as follows:

- 42 percent said the technology is still too immature to justify investment

- 36 percent cited a lack of employee training

- 36 percent cited privacy concerns

The international survey tells a harder story overall. Among the nearly 6,000 executives surveyed across four countries, 89 percent reported no impact of AI on their labor productivity over the past three years. More than 90 percent reported no impact on employment. These are not fringe firms or laggards; they include companies already using AI in various forms.

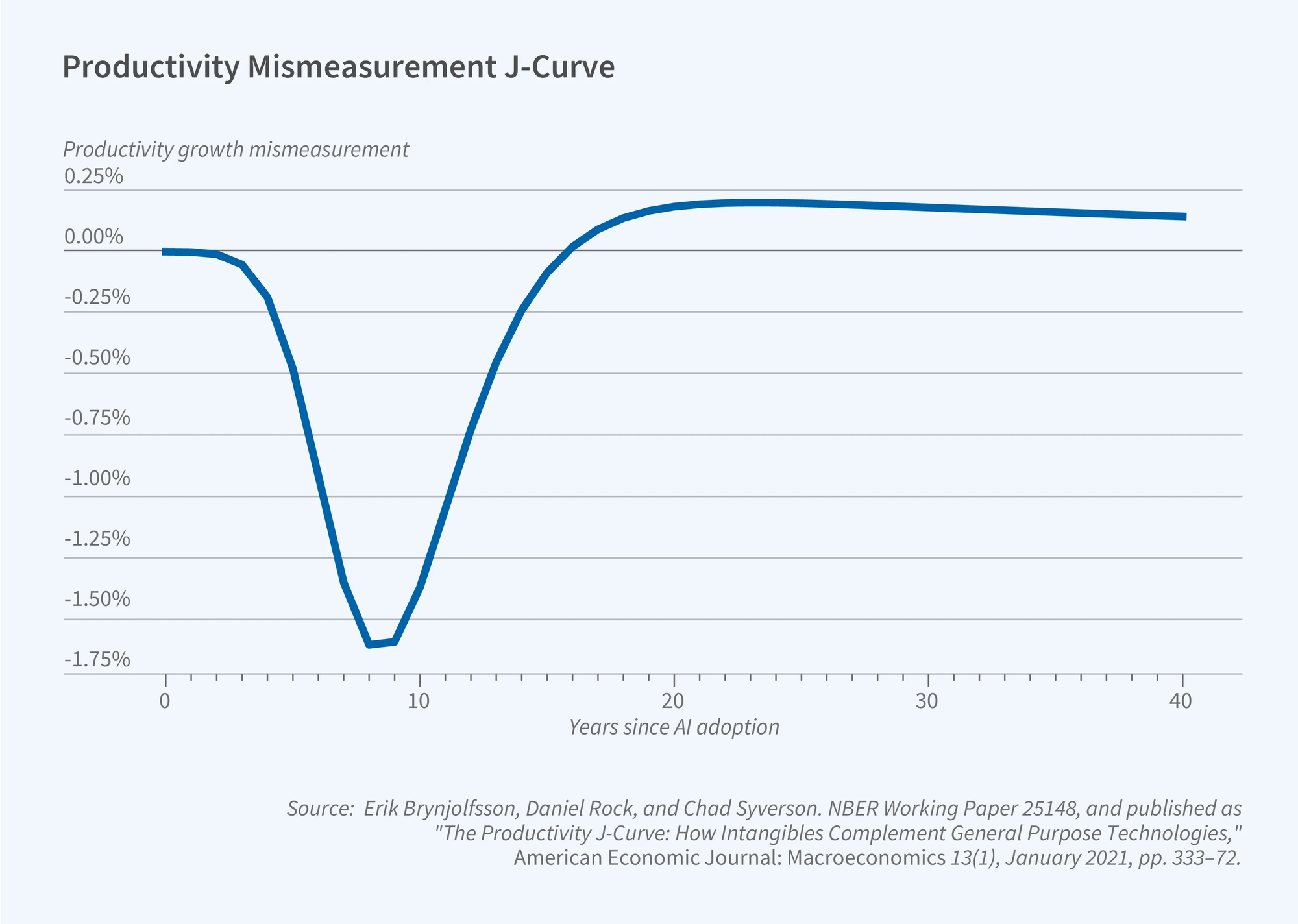

The Productivity Paradox Is Back

The CFO-focused paper documents what it explicitly calls a productivity paradox: executives consistently report larger perceived productivity gains than those reflected in actual revenue data.

This pattern has precedent. Economist Robert Solow observed in 1987 that the computer age was everywhere except in the productivity statistics, a dynamic that held for more than a decade before the IT productivity surge of the late 1990s and early 2000s finally materialized. The NBER researchers draw the parallel directly, noting that "transformative technologies are widely viewed as important well before their effects are fully reflected in measured productivity."

The gap between perceived and measured gains likely reflects two things: delayed output realization, since efficiency improvements may take time to translate into revenue, and quality improvements that standard productivity metrics do not fully capture.

Erik Brynjolfsson, writing in the Financial Times in February 2026, argued that the AI productivity take-off is now becoming visible in US macroeconomic data. New Bureau of Labor Statistics benchmark revisions showed total payroll growth revised downward by approximately 403,000 jobs, while real GDP remained robust at 3.7 percent in Q4. His analysis suggests US productivity grew roughly 2.7 percent in 2025, nearly double the 1.4 percent annual average of the prior decade. That macro signal has not yet shown up consistently in firm-level survey data, which is precisely what a lagged technology transition would predict.

What AI Is Actually Being Used For

Among firms that have invested in AI, the primary motivations were improving production efficiency and labor productivity rather than cost reduction. The largest reported benefits aligned with those motivations: improving production efficiency, enhancing decision-making speed, and enhancing output quality.

Cost reduction and headcount reductions ranked lower as both motivations and realized benefits. The data from CFOs paints a more nuanced picture than the dominant public narrative around AI, which tends to center on job displacement, at least for the current moment.

Gains are not primarily driven by capital investment in hardware or software. The paper finds they instead reflect increases in what it describes as revenue-based total factor productivity, associated with innovation and demand-oriented channels: developing new products, reaching customers more effectively, and improving the quality of outputs.

Complementary investments matter significantly. European comparison data cited in related research found that each additional percentage point spent on workforce training added 5.9 percentage points to productivity gains. Software and data infrastructure added 2.4 percentage points. Firms investing in AI without corresponding investment in training and infrastructure are not seeing the same returns.

The Employment Question: A Divergence in Expectations

Executives surveyed in the international study predict that AI will cut employment by 0.7 percent at their firms over the next three years. Employees at the same firms predict a 0.5 percent increase in employment over the same period. These two groups are looking at the same technology, in the same companies, and arriving at opposite conclusions about its workforce implications.

The CFO-focused paper finds that near-term aggregate employment effects are small. Firms reported a negligible impact from AI on headcounts in 2025, and the average anticipated impact on 2026 employment is also close to zero. However, one subset of firms, specifically large companies, expects to reduce employment by 0.8 percent in 2026 as a result of AI.

The workforce composition shift may be more significant than the headline employment number. Large companies anticipate a shift away from routine clerical roles toward skilled technical jobs. The paper projects that routine clerical employment will decline by more than 2 percentage points over three years, partially offset by increases in engineers, data analysts, and scientists.

The implication is not mass unemployment but a structural reallocation. The workers in the most directly affected categories are not the same workers who would fill the technical roles expected to grow, and that mismatch is where the distributional pressure will likely concentrate.

The Expectations Horizon: Why Executives Are Still Optimistic

Despite reporting minimal productivity gains over the past three years, the same executives predict meaningful impacts over the next three. Across the international survey, firms forecast AI will boost productivity by 1.4 percent, increase output by 0.8 percent, and cut employment by 0.7 percent within three years.

The CFO survey shows that small and large companies alike expect larger effects in 2026 than they experienced in 2025. Expected productivity gains from AI increased from 1.5 percent in February through April 2025 to 1.9 percent in November 2025 through January 2026.

Whether these expectations materialize depends on factors that are not yet resolved: whether the technology's capabilities continue to improve at the pace of the past two years, whether firms manage the complementary investments in training and infrastructure that appear to be necessary preconditions for gains, and whether the macroeconomic environment allows firms to capture the efficiency benefits they are already observing internally as revenue.

The Solow paradox eventually resolved. IT investment that seemed to produce no aggregate productivity gains through the 1980s and early 1990s eventually showed up as a sustained productivity surge. The NBER researchers are implicitly betting that AI follows the same arc.

What the Research Means for Businesses

The divide between large and small firms is the finding with the most direct business implications. Large firms are investing at a scale that small firms are not approaching. Thirty percent of large firms expect to spend more than $1 million on AI in 2026. Most small firms are not at one-twentieth of that investment level. Over time, that gap in capability will likely widen into a gap in competitive position, particularly in industries where AI-enhanced productivity compounds across functions.

For small businesses, the barrier is not primarily cost. The most-cited reasons for not investing are technology immaturity and a lack of employee training, not budget. Forty-two percent of non-adopters say the technology is not yet mature enough. Thirty-six percent point to training gaps. Both are actionable constraints rather than permanent ones.

For large firms already seeing productivity gains, the research suggests those gains likely understate the eventual impact. The productivity paradox finding, where executives perceive larger gains than revenue data captures, is consistent with the early stages of a technology transition where operational efficiency is improving before the revenue implications are fully visible.

Wrap up

The NBER research does not support either the most optimistic or the most pessimistic narratives about AI and productivity. It supports something more specific: AI is delivering real but modest gains now, concentrated at larger and more sophisticated firms, with a reasonable expectation that those gains will accelerate as adoption deepens and the complementary investments required to realize them become more widespread.

The firm-size gap is the most consequential structural finding. If large firms continue to invest at current rates while small firms remain at the threshold of meaningful adoption, the productivity divergence between them will grow. Whether that translates into wider market concentration, or whether the democratization of AI tools eventually closes the gap, is a question the current data cannot answer definitively. What it can say is that the gap is real, measurable, and widening.

Frequently Asked Questions

What did the NBER research find about AI productivity gains overall?

Two NBER-affiliated papers published in early 2026 found that AI is delivering real but modest labor productivity gains, primarily concentrated in high-skill services and finance. Firms in those sectors are seeing implied annual labor productivity growth of approximately 0.8 percent, while manufacturing and lower-skill services are seeing gains of around 0.4 percent. However, 89 percent of the nearly 6,000 executives surveyed in the international study reported no impact on productivity over the past three years. The gains are real but distributed very unevenly.

Why are large companies so far ahead of small businesses on AI?

Investment scale is the primary driver. Around 30 percent of large firms expect to invest more than $1 million in AI in 2026, compared to 1 percent of small firms. Nearly 60 percent of small firms plan to invest less than $20,000. Large firms also have dedicated technical staff, established data infrastructure, and the organizational capacity to manage complex deployments. Smaller firms cite technology maturity, employee training gaps, and privacy concerns as the main barriers to adoption.

What is the productivity paradox and why does it matter here?

The productivity paradox refers to the observation that transformative technologies are widely perceived as important before their effects show up in measured productivity data. Economist Robert Solow identified this pattern in the 1980s with computing. The NBER research documents a similar gap today: CFOs report productivity gains from AI that are substantially larger than revenue-based measures would suggest. The researchers argue this reflects delayed output realization and quality improvements that standard metrics do not capture. The precedent from the IT era is that the gains eventually materialized, roughly a decade after adoption began.

What do the surveys say about AI and employment?

Near-term aggregate employment effects appear small. Firms reported negligible headcount impacts in 2025, and average anticipated impacts for 2026 are close to zero overall. However, large firms expect to reduce employment by approximately 0.8 percent in 2026. The more significant shift appears to be compositional: routine clerical employment is expected to decline by more than 2 percentage points over three years, with offsetting growth in skilled technical roles including engineers, data analysts, and scientists.

Why do executives and employees disagree about AI's employment impact?

The international survey found a striking divergence: executives predict AI will cut employment by 0.7 percent at their firms over three years, while employees at the same firms predict a 0.5 percent increase in employment. The paper describes this as a sizable gap in expectations. Executives may see how AI is being deployed at the task and workflow level, while employees may expect productivity gains to translate into growth rather than headcount reduction.

What types of AI are businesses actually using?

The most commonly cited uses across the international survey are text generation using large language models, followed by visual content creation and data processing using machine learning. Among firms that have adopted AI, the primary motivations were improving production efficiency and labor productivity, with cost reduction ranking lower. The biggest realized benefits included improving production efficiency, enhancing decision-making speed, and enhancing output quality.

Is the AI productivity effect visible in the broader economy yet?

Macro-level evidence is becoming more encouraging. Erik Brynjolfsson, writing in the Financial Times in February 2026, pointed to revised Bureau of Labor Statistics data showing US productivity grew approximately 2.7 percent in 2025, nearly double the prior decade's average. Firm-level survey data, however, still shows the majority of companies reporting no impact to date, consistent with a technology transition that is underway but not yet broadly realized.

What actually drives AI productivity gains according to the research?

The gains are not primarily driven by capital investment in hardware or software. They reflect increases in revenue-based total factor productivity, associated with innovation and demand-oriented channels including new product development and improved customer engagement. Complementary investments are critical: related European data found that each additional percentage point spent on workforce training added 5.9 percentage points to productivity gains. Firms investing in AI without corresponding investment in training and infrastructure are not seeing the same returns.

Related Articles