Something unusual happened to enterprise software in early 2026: stocks started falling even when companies beat earnings.

On January 29, ServiceNow reported $3.47 billion in subscription revenue, up 21% year-over-year, raised its full-year guidance, and posted its ninth consecutive earnings beat. The stock fell 11% in the session. The same morning, Microsoft reported $81.3 billion in quarterly revenue, beating estimates. It shed $357 billion in market capitalization by the close.

Nine straight earnings beats, guidance raised, and yet the stock was crushed. The market was not reacting to financial performance but repricing a business model entirely.

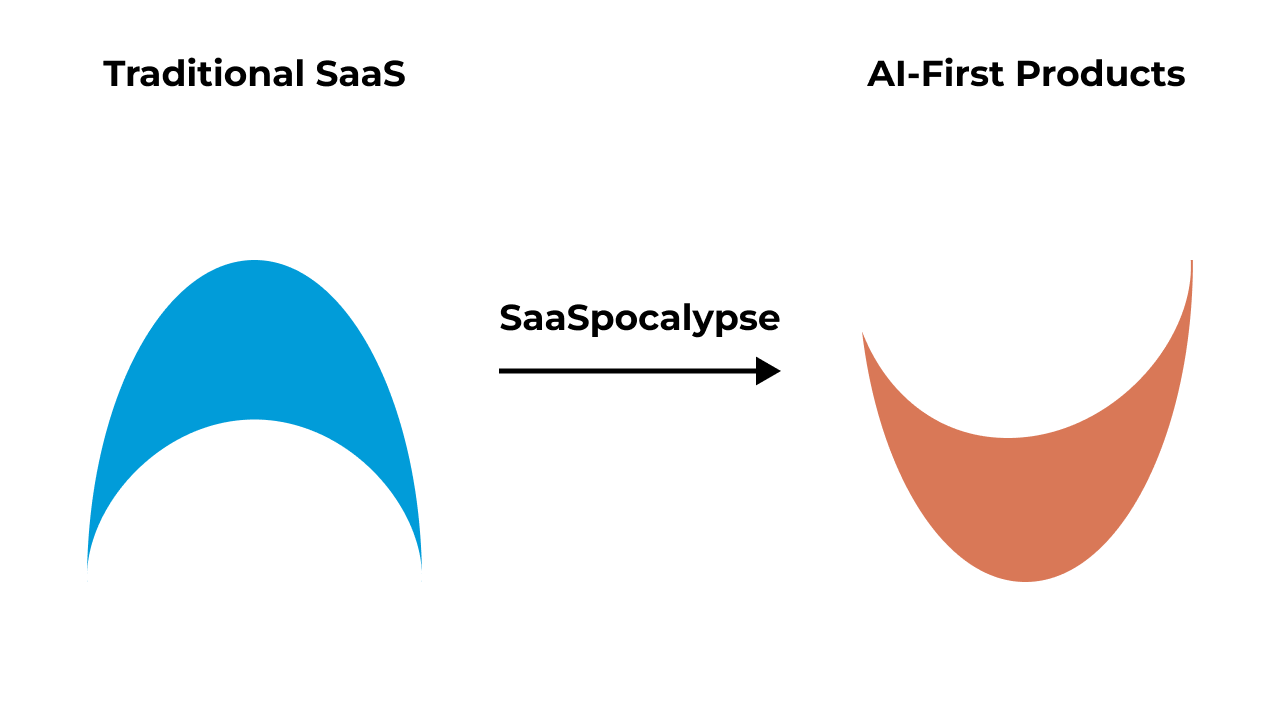

What Is the SaaSpocalypse

Wall Street coined the term in early 2026 to describe the rolling selloff in enterprise software stocks triggered not by disappointing earnings but by a structural fear: that AI agents are about to render the per-seat licensing model obsolete.

The iShares Expanded Tech-Software ETF, ticker IGV, fell more than 21% year-to-date through late March, and reached 27% below its January 1 level by April 9, according to Bloomberg. A separate index of SaaS stocks recorded a year-to-date decline approaching 40% by mid-April. Total market capitalization wiped from the software sector since January exceeded $2 trillion, according to analysis from Bulloak Capital, making it a bigger relative decline than the software sector experienced during the Global Financial Crisis, exceeding both the dot-com bust's relative drawdown and the 2022 rate-hike shock, according to SaaStr's market analysis.

Software forward price-to-earnings multiples, which averaged 84.1x during the 2020 to 2022 peak, fell to 22.7x by early 2026. For the first time in the history of cloud computing, software now trades at a discount to the S&P 500 overall market multiple.

The Catalysts: What Actually Triggered the Selloff

The SaaSpocalypse did not have a single clean trigger but unfolded through a sequence of events across four months.

Late 2025: The early warning signs. Salesforce reported a rare revenue miss in late 2025, followed by weak guidance for the 2026 fiscal year. For a company that has functioned as the bellwether of enterprise software, the miss reverberated across the sector. Investors began asking whether something structural had changed in enterprise software purchasing behavior.

January 2026: The day software broke. On January 29, OpenAI released Project Operator. Within hours, the sector was in freefall. The product demonstrated AI agents executing complex, multi-step business workflows autonomously, without a human logging into a dashboard to manage the process. It was the first widely distributed demonstration that AI was transitioning from copilot to operator.

February 2026: The Anthropic Effect. On February 24, Anthropic launched Claude Cowork. The product demo showed AI agents handling legal document review, financial analysis, customer support triage, and project management end-to-end. These are precisely the categories where SaaS companies charge $20 to $150 per seat per month.

Within 48 hours, approximately $285 billion in SaaS market capitalization vanished. Thomson Reuters posted its largest single-day decline on record, down 15.83%. LegalZoom fell 19.68%. The iShares software ETF recorded its worst two-day decline since 2008.

March to April 2026: The ratchet effect. On April 9, Cloudflare fell 12%, Snowflake fell 9%, ServiceNow fell 7%, and Salesforce slid 4% in a single session. A Bloomberg report cited two factors: AI app software disruption and private credit concerns for software. Hedge funds had shorted approximately $24 billion in software stocks by that point.

Why Per-Seat Pricing Is the Core of the Fear

The per-seat model was elegant in its simplicity. When a company grew headcount, it needed more software seats, and when enterprises expanded, SaaS revenue expanded automatically. The link between human hiring and software spending was structural, predictable, and highly durable.

AI agents break that link at the mechanism level, and the arithmetic is direct. If 10 AI agents can perform the work of 100 sales representatives, a company no longer needs 100 Salesforce seats. It needs 10, or perhaps none, depending on how the workflow is structured, which Jason Lemkin of SaaStr described as a structural reversal of the growth engine rather than a cyclical slowdown in software purchasing.

The math was never subtle. Every dollar going to AI infrastructure, AI tooling, and AI headcount is a dollar not going to another Salesforce seat, another Workday module, or another ServiceNow add-on. The hyperscalers will spend more than $470 billion on AI infrastructure in 2026 alone. That money came from somewhere, and enterprise IT budgets are a large part of where.

The Actual Damage: What Happened to Specific Companies

The selloff was not uniform but sorted the sector ruthlessly by business model vulnerability.

The Atlassian number deserves emphasis. In March 2026, Atlassian reported its first-ever decline in enterprise seat counts. For a company whose entire growth model depends on seat expansion, a reversal in that metric is an earthquake regardless of where current revenue stands.

The Bear Case: Why Some Analysts Think This Is Just the Beginning

The most aggressive read on the SaaSpocalypse is not that valuations overreacted but that they have not yet caught up with the structural reality.

UBS cut ServiceNow to Neutral with a $100 price target, a level that implied further significant downside from April prices, saying the April 9 selloff was "just the beginning" of a longer repricing.

Rolf Bulk, tech equities analyst at Futurum Group, told CNBC that there "is likely to be cannibalization of SaaS by AI-driven workflows and that will impact the multiple the sector trades on." His view was not that SaaS companies would disappear but that the premium multiple they have commanded for two decades is no longer justified.

The structural argument goes further. SaaStr's analysis points out that public SaaS growth rates have declined every single quarter since the 2021 peak. The AI narrative gave the market permission to reprice what the actual revenue numbers had been indicating for three years. Strip out price increases on captive customers, and net new customer numbers have been weak across the board for multiple quarters.

An estimated 40% of IT budgets are being reallocated from traditional SaaS subscriptions to agentic platforms and LLM token usage, according to surveys of enterprise CIOs cited in March 2026 reporting. Enterprise software multiples have already compressed from an EV/Sales average of 5.6x at the end of 2025 to approximately 4.2x by mid-March.

The Bull Case: Why Goldman and JPMorgan Called It Overdone

Not everyone agreed with the bear case, and several credible voices made substantive counterarguments that deserve equal weight.

Goldman Sachs CEO David Solomon called the SaaS selloff too broad, arguing the market was not differentiating between companies that would be disrupted by AI and those that would benefit from it. JPMorgan echoed this view, noting an overly bearish outlook and the potential for a software rebound.

Wedbush Securities argued that enterprises will not overhaul tens of billions of dollars of prior software infrastructure investment to migrate to Anthropic or OpenAI, noting that large enterprises took decades to accumulate the data and workflows embedded in their current software. Arm Holdings CEO Rene Haas described the market fears as "micro-hysteria" in comments to the Financial Times.

The most compelling counterargument came from SaaStr founder Jason Lemkin, who made a precise claim: nobody is building a homegrown CRM in Replit to replace Salesforce. Enterprise systems of record, the databases and compliance-ready infrastructures that hold the organizational data SaaS companies have accumulated, are not replaceable by a general-purpose AI prompt. Shipping a functional app with vibe coding, Lemkin argued, is approximately 2% of the work involved in running an enterprise software platform.

Dan Ives, a prominent tech investor, called the software selloff a "generational buy," arguing that enterprise switching costs and data lock-in will protect established players longer than the market assumes.

Who Is Winning and Who Is Losing

The selloff has begun sorting the sector into three distinct groups: survivors with deep data moats, adapters pivoting to new pricing, and structural casualties whose business model cannot be defended.

The survivors are the companies whose value is embedded in proprietary data, compliance infrastructure, and deep system-of-record integration. Oracle, despite being down approximately 25% year-to-date, has a data moat that makes AI replacement technically complex. Its Q1 RPO data showed continued enterprise commitment. SAP, down 15% following a disappointing cloud revenue forecast, sits at the center of global ERP infrastructure that cannot be displaced by an AI agent without years of migration work.

The adapters are the companies that moved fastest toward outcome-based pricing. ServiceNow introduced a tier of Agentic Annual Contract Value, charging customers for tasks completed by AI agents rather than for human login credentials. The company recovered nearly half of its Q1 losses through April as investors rewarded the pivot. Gartner data shows that 40% of enterprise SaaS contracts now include outcome-based elements, up from 15% two years ago.

The structural casualties are the companies whose products map cleanly to human task completion, whose data moats are shallow, and whose pricing model cannot survive the transition. Vertical SaaS companies built around specific workflows are most exposed, with legal tech, HR tools, marketing automation, and document management platforms facing AI agents that do not just threaten the pricing model but the product category itself.

The Pricing Model in Transition

The clearest operational signal that something structural is changing is the pricing model transformation now underway across the sector, moving from per-seat licenses toward three distinct alternatives.

Usage-based pricing, where customers pay for API calls or compute consumed, removes the per-human anchoring. Outcome-based pricing, where customers pay per resolved ticket, per contract reviewed, or per lead qualified, moves value capture to results rather than access. Consumption-based pricing, which tracks actual activity rather than licensed seats, more accurately reflects AI agent usage than a headcount-derived license.

Adobe has already shifted toward Generative Credit pricing. ServiceNow's Agentic ACV tier is outcome-based by design. Salesforce has been publicly signaling a shift toward AI-driven pricing. None of these transitions are painless: they require repricing existing customer bases, rebuilding sales compensation structures, and renegotiating contracts at lower per-unit economics, with the bet that volume growth offsets the margin pressure.

Conclusion

The SaaSpocalypse is not primarily a story about AI killing software but about AI killing the humans who used the software, and by extension the per-seat revenue model those humans generated. The distinction matters because it changes the recovery path entirely.

Software companies that own proprietary data, provide compliance infrastructure, and sit at the center of critical business workflows will survive the transition, though their multiples will never return to 84x forward earnings. Companies whose products exist as interfaces for human task completion, with no data moat and no system-of-record status, face a genuinely structural challenge that the current valuations may not fully reflect.

The $2 trillion in destroyed market capitalization is not all justified, and not all unjustified. The market is working through a sorting process that will take several years to complete. The companies that come out on the other side will look different from the ones that entered the cloud era, and the ones that do not adapt will not come out at all.

Frequently Asked Questions

What is the SaaSpocalypse?

The SaaSpocalypse is the term Wall Street analysts and financial media coined in early 2026 to describe the rolling selloff in enterprise software stocks. The iShares software ETF IGV fell more than 21% year-to-date through late March 2026, and more than $2 trillion in software market capitalization was wiped out. The selloff was triggered by fears that AI agents would replace the human workers who generate per-seat SaaS licensing revenue, undermining the business model at its foundation.

What triggered the SaaSpocalypse?

The selloff built through a sequence of events beginning with Salesforce's rare revenue miss in late 2025, accelerating on January 29, 2026, when OpenAI released Project Operator, and reaching its initial climax when Anthropic launched Claude Cowork on February 24, 2026. The Claude Cowork demo showed AI agents handling legal document review, financial analysis, and project management end-to-end, wiping $285 billion in SaaS market value within 48 hours.

Which SaaS companies were hit hardest?

The hardest-hit companies were those whose revenue depended on per-seat licensing for task-level human work. Salesforce fell approximately 30% year-to-date. Workday and Atlassian each fell 40% or more. Adobe was down 30%. ServiceNow fell approximately 40% before partially recovering after pivoting to outcome-based pricing. Atlassian reported its first-ever decline in enterprise seat counts.

Is the SaaS selloff a temporary overreaction or a structural repricing?

Both views have credible support. Goldman Sachs, JPMorgan, and Wedbush Securities argued the selloff was too broad and that enterprise switching costs and data moats will protect established players. UBS, Futurum Group analysts, and SaaStr argued the repricing reflects a genuine structural shift, noting that SaaS growth rates had been declining for three years and the AI narrative gave the market permission to reprice what revenue trends had been indicating for some time.

What is the alternative to per-seat SaaS pricing?

Three models are emerging. Usage-based pricing charges for API calls or compute consumed rather than licensed seats. Outcome-based pricing charges per completed task, such as per contract reviewed or per support ticket resolved. Consumption-based pricing tracks actual activity regardless of headcount. Gartner data shows that 40% of enterprise SaaS contracts now include outcome-based elements, up from 15% two years ago. ServiceNow's Agentic ACV tier and Adobe's Generative Credit pricing are among the most visible examples of the transition.

Related Articles