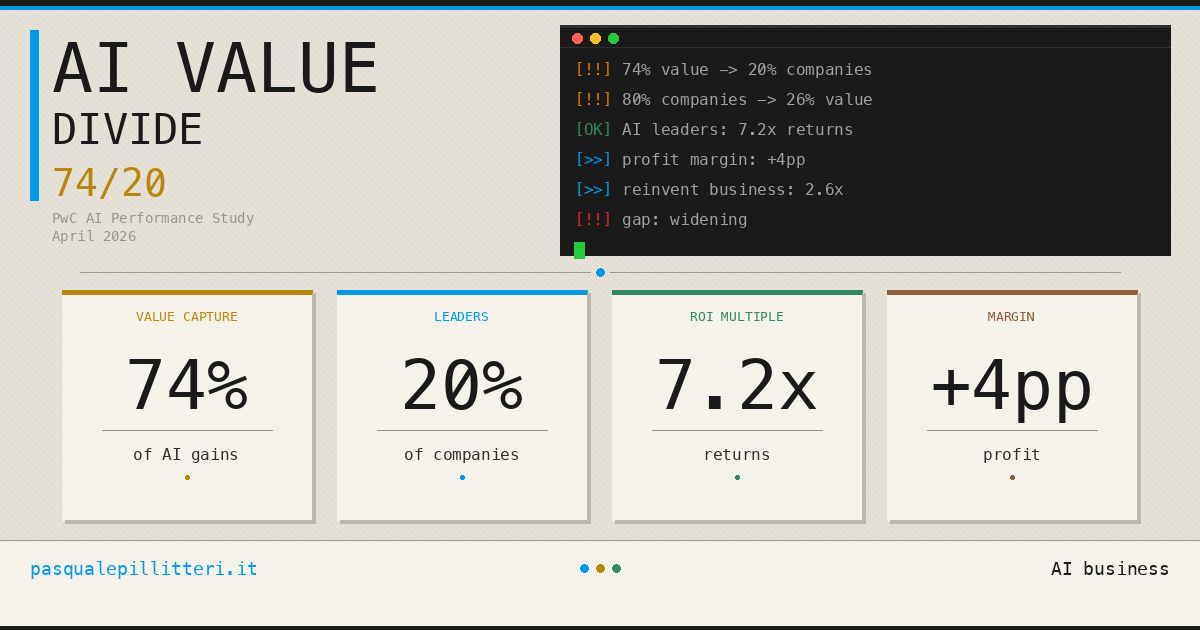

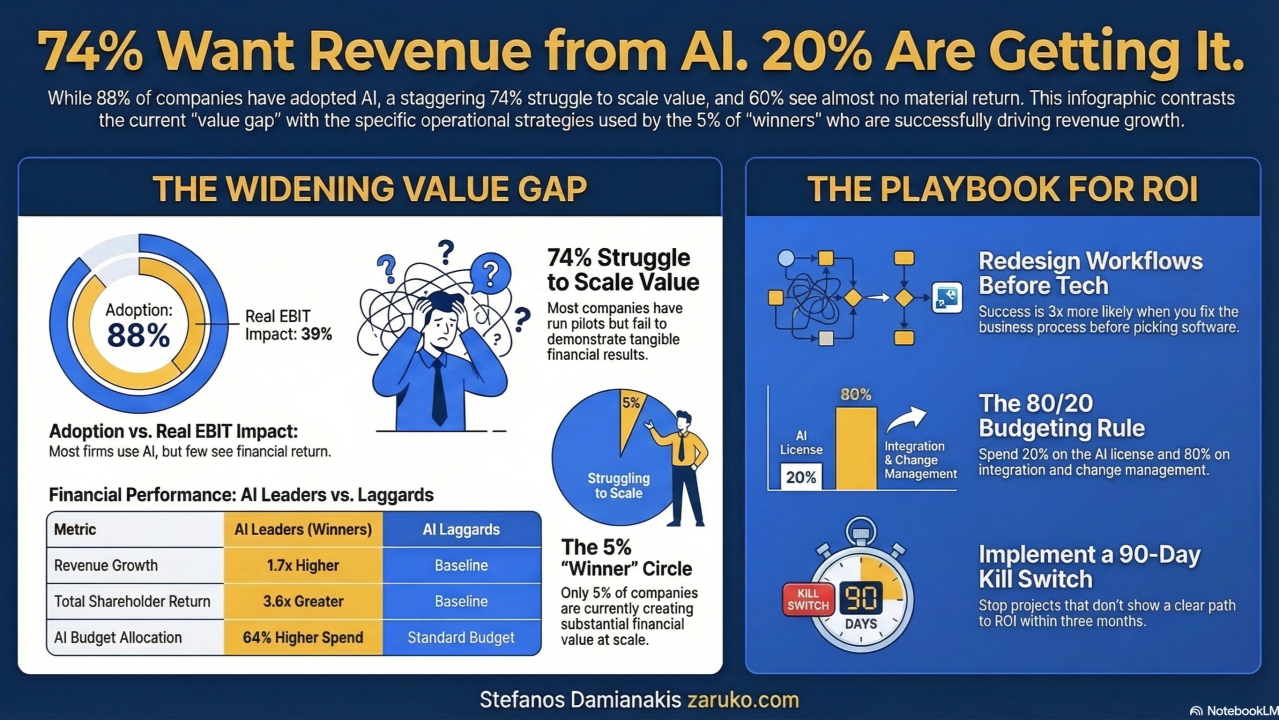

Most companies using AI are running pilots. A small group is running businesses that look fundamentally different from their competitors. According to PwC's 2026 AI Performance Study, released April 13, that split produces a stark result: 74% of AI's economic value is captured by just 20% of organizations.

The study surveyed 1,217 senior executives at large, publicly listed companies across 25 sectors and multiple regions. It measured AI-driven performance as the combined revenue and efficiency gains attributable to AI, adjusted against industry medians. The top-performing 20% of companies are generating 7.2 times more AI-driven revenue and efficiency gains than the average competitor.

The divide is not primarily about how much AI these companies deploy but about what they point AI at.

The Core Finding: Growth vs. Cost Reduction

PwC's study identifies the single strongest predictor of AI-driven financial performance, and it is not automation, not efficiency, and not cost reduction. It is industry convergence: using AI to identify and pursue growth opportunities arising as industry boundaries dissolve.

Leading companies are two to three times more likely than peers to say they use AI to identify and pursue growth opportunities linked to industry convergence, such as collaborating with partners outside their core sector. They are 2.6 times more likely to report that AI has improved their ability to reinvent their business model.

Joe Atkinson, Global Chief AI Officer at PwC, described the pattern directly: "Many companies are busy rolling out AI pilots, but only a minority are converting that activity into measurable financial returns. The leaders stand out because they point AI at growth, not just cost reduction, and back that ambition with the foundations that make AI scalable and reliable."

PwC's own framing on its analysis page captures the distinction: "Plenty of companies use AI to become more efficient at the work they already do. Think of insurance firms, where AI solutions rapidly process claims, or software makers, where programmers direct AI to write a substantial portion of new code. The AI leaders we studied use AI for efficiency, too. But they don't stop there. These companies treat AI like a top-line-boosting reinvention engine."

The AI Fitness Index: What the Top 20% Have That Others Don't

PwC analyzed the impact of 60 AI management and investment practices in the study, grouping them into two categories: AI use (how companies apply AI) and AI foundations (the infrastructure, governance, data quality, and talent that make AI deployable at scale). Together these form what PwC calls the AI Fitness Index.

The research consistently shows that foundations matter as much as scale, and leaders share several characteristics that the majority of AI users lack.

- Workflow redesign, not tool layering. Companies generating the strongest AI returns are twice as likely to redesign workflows around AI rather than simply adding AI tools to existing processes. The distinction matters: layering a chatbot on a broken process does not improve the process. Redesigning the process around AI capabilities does.

- Portfolio discipline. Top performers actively prune underperforming AI initiatives. Only 28% say they conduct AI portfolio reviews to a "large" or "very large" extent, meaning even leaders have room to improve here. The broader population is far less disciplined about stopping what is not working.

- Enterprise-wide integration. CEOs who have embedded AI extensively across products, services, demand generation, and strategic decision-making are two to three times more likely to report both cost and revenue gains. Isolated departmental deployments produce fragmented results.

- Responsible AI frameworks. Companies that have established governance and Responsible AI structures are three times more likely to report meaningful financial returns. According to PwC's analysis, governance is not just a compliance function but correlates directly with financial performance, because it enables the kind of consistent, reliable deployment that produces measurable results at scale.

The CEO Survey Context: Most Leaders Haven't Seen the Returns

The AI Performance Study lands alongside a broader pattern in PwC's enterprise research. Three months earlier, PwC's 29th Global CEO Survey, based on responses from 4,454 CEOs across 95 countries, found that only one in eight CEOs (12%) say AI has delivered both cost and revenue benefits. Overall, 33% report gains in either cost or revenue, while 56% say they have seen no significant financial benefit to date.

CEO confidence in revenue growth fell to a five-year low, with just 30% expressing confidence about their company's revenue prospects for the next 12 months, down from 38% in 2025 and 56% in 2022. AI was explicitly cited as a defining fault line.

PwC Global Chairman Mohamed Kande said at Davos: "2026 is shaping up as a decisive year for AI. A small group of companies are already turning AI into measurable financial returns, while many others are still struggling to move beyond pilots."

The 74/20 finding from the April performance study is essentially the structural explanation for why CEO confidence has dropped. Most companies are spending on AI without seeing returns, not because the technology does not work, but because the majority of AI activity is concentrated in pilots that never scale into the core business.

The Pilot Trap

PwC's language throughout its research is consistent about the pattern it describes. Companies get stuck in what the firm calls "pilot mode": AI initiatives exist, reports are produced, activity is visible, but measurable financial returns do not materialize.

The reasons PwC identifies for this trap are structural rather than technological:

The most common AI mistake, according to PwC's 2026 AI Predictions, is a ground-up rather than top-down approach. Organizations crowdsource AI ideas from teams and then try to assemble them into a strategy. The result is a portfolio of initiatives that may not match enterprise priorities, are executed with uneven discipline, and almost never lead to transformation — adoption numbers look impressive while business outcomes do not follow.

The technology itself delivers roughly 20% of an AI initiative's value, according to PwC. The remaining 80% comes from redesigning work so that AI agents can handle routine tasks and humans focus on what drives genuine impact. Most organizations invest heavily in the 20% (tools, models, API access) and underinvest in the 80% (workflow redesign, governance, workforce reskilling, and outcome measurement).

Industry Convergence: The Overlooked Opportunity

PwC's identification of industry convergence as the single strongest factor in AI performance is the finding that most deserves unpacking, because it is the least intuitive of the study's conclusions.

Industry convergence describes what happens when AI enables companies to operate in adjacent markets they could not previously access, such as a financial services firm entering health insurance, a retailer deploying AI-powered logistics services to other businesses, or a media company building AI-driven personalization that becomes a product sold to healthcare providers. These are real patterns PwC's research captures.

The mechanism is straightforward: AI reduces the marginal cost of entering adjacent markets, because the same underlying capabilities (data processing, prediction, generation, automation) transfer across industries more readily than traditional operational capabilities do. Companies that recognize this and deliberately pursue cross-industry growth opportunities are capturing value that their competitors, who are focused on efficiency gains within existing business lines, cannot see.

The report's authors are explicit that this is the differentiating factor: capturing growth opportunities from industry convergence is the single strongest element in PwC's AI fitness index, ahead of efficiency gains, ahead of cost reduction, and ahead of individual technology investments.

What This Means for the 80%

The PwC study is not primarily a story about the 20% who are winning but about the 80% who are not, and about whether the gap is temporary or structural.

PwC's own assessment is that the gap is likely to widen. "Without a shift in approach, the performance gap between AI leaders and laggards is likely to widen further as leading companies continue to learn faster, scale proven use cases and automate decisions safely at scale." The compounding effect of learning faster means the lead grows non-linearly: companies six months ahead in AI maturity will be further ahead still in eighteen months, not the same distance.

For organizations in the 80%, the PwC prescription is narrower than it might appear. The study's advice is not to deploy more AI but to deploy focused AI: identify a small number of workflows or business processes where AI can produce large payoffs, fund those thoroughly, and scale the winners before expanding. The alternative, which is the current state for most organizations, is a broad portfolio of initiatives at low investment levels that produces impressive activity metrics and minimal returns.

The specific practices the study recommends for organizations not yet in the leading group include:

- Anchor AI investments to a small set of priority outcomes. Define what business result each initiative must produce before funding it. Outcome metrics should be concrete, financial, and measurable.

- Redesign workflows rather than augmenting them. The highest returns come from replacing a multi-step process with an AI-first workflow, not from adding AI assistance to an existing process.

- Build governance before scaling. Organizations that establish responsible AI frameworks before broad deployment are three times more likely to see meaningful returns. Governance built after problems emerge is more expensive and less effective.

- Treat industry convergence as a strategic question. The performance data suggests that companies asking only "how can AI make us more efficient?" are missing the higher-value question: "what adjacent markets can AI now make viable for us?"

Wrap up

The 74/20 split in AI returns is not a technology failure but an organizational design and strategic orientation failure. The AI tools available to the leading 20% of companies are largely the same tools available to everyone else. What differs is whether those tools are pointed at operational efficiency, which many organizations share, or at growth and business model reinvention, which the majority have not yet attempted.

PwC's CEO survey data shows that most business leaders know something is not working: only 12% have seen AI deliver both cost and revenue gains, CEO confidence in revenue growth is at a five-year low, and the industry is spending heavily on technology that is producing results for a small minority.

The gap between organizations that are capturing AI's value and those that are not is widening, not converging. Companies that have not yet built the foundations that enable scalable AI deployment, and that have not shifted their AI strategy from efficiency to growth, are not simply behind on a curve that will eventually flatten out.

They are running a different race with a different finish line.

Frequently Asked Questions

What is PwC's 2026 AI Performance Study?

PwC's 2026 AI Performance Study, released April 13, 2026, is a global survey of 1,217 senior executives at large, publicly listed companies across 25 sectors and multiple regions. It measures AI-driven performance as the combined revenue and efficiency gains attributable to AI, adjusted against industry medians. PwC analyzed the impact of 60 AI management and investment practices, grouped into AI use and AI foundations, which together form the AI Fitness Index.

Why are only 20% of companies capturing 74% of AI's economic value?

PwC's analysis finds the difference is primarily strategic rather than technological. Leading companies use AI as a growth and reinvention engine, pursuing new revenue opportunities, particularly from industry convergence. The majority of organizations focus AI primarily on cost reduction and efficiency within existing business lines. The leaders also have stronger AI foundations: more disciplined governance, workflow redesign rather than tool layering, and enterprise-wide integration rather than fragmented pilots.

What is industry convergence and why does it matter for AI returns?

Industry convergence describes using AI to pursue growth opportunities in adjacent markets outside a company's core sector. PwC's study identifies this as the single strongest factor in AI-driven financial performance, ahead of efficiency gains and cost reduction. AI reduces the marginal cost of entering adjacent markets because the underlying capabilities transfer across industries, giving companies that recognize this an advantage unavailable to those focused only on their existing business lines.

What is the AI Fitness Index?

PwC's AI Fitness Index is the combined score of 60 AI management and investment practices, grouped into two categories: AI use (how the company applies AI) and AI foundations (the infrastructure, governance, data quality, and talent that enable scalable deployment). Companies with strong scores on the index are three times more likely to report meaningful financial returns from AI.

What does PwC's CEO survey say about AI returns?

PwC's 29th Global CEO Survey, based on 4,454 CEO responses across 95 countries, found that only 12% of CEOs say AI has delivered both cost and revenue benefits. Overall, 56% have seen no significant financial benefit to date. CEO confidence in revenue growth fell to its lowest level in five years, with 30% expressing confidence about the next 12 months, down from 38% in 2025.

Related Articles