For decades, utility stocks were the financial equivalent of a savings bond: predictable, unsexy, and something you bought when you wanted to stop thinking about your portfolio. Analysts described the sector with phrases like "defensive haven" and "dividend income." Growth investors ignored them entirely.

That era ended somewhere around 2023, and the cause was a single sector: artificial intelligence.

New consensus forecasts released in April 2026 project 15.9% earnings growth for global infrastructure companies this year, a figure that, according to FinancialContent's analysis, dwarfs the sector's historical low-single-digit averages. The Morningstar US Utilities Index finished 2025 up 19%, and has surged 70% from its low in late 2023. NRG Energy was up nearly 80% by mid-November 2025, almost double the gain of Nvidia over the same period.

The bottleneck in the AI era, it turns out, is not chips. It is kilowatts.

Why AI Changed Everything for Power Companies

The energy math behind modern AI is staggering. A single AI-related task can consume up to 1,000 times more electricity than a traditional web search. Training GPT-4 required as much electricity as 10,000 US homes use in an entire year. Nvidia's H100 chips generate 700 watts of heat each. A single Meta AI training cluster packs 24,000 GPUs into one facility.

US data center electricity demand is projected to triple between 2024 and 2030, eventually consuming around 10% of the nation's total power, according to Morningstar's forecasts. Goldman Sachs projects data center power demand will grow 160% by 2030. The International Energy Agency estimates that by 2030, data centers could consume as much electricity as Japan does today.

The hyperscalers are spending accordingly. Meta, Microsoft, Amazon, and Alphabet are projected to spend $700 billion on AI infrastructure in 2026 alone, with roughly 100 gigawatts of new data centers expected to come online between 2026 and 2030.

All of that infrastructure needs a continuous, reliable power supply, and the US grid was not built for it.

Data Center Power Demand: The Scale of the Shift

| Metric | Figure |

|---|---|

| AI task vs. web search energy use | Up to 1,000x more |

| US data center demand projected change (2024-2030) | Triple |

| US data center share of total electricity by 2028 | Up to 12% |

| Goldman Sachs data center power demand growth by 2030 | 160% |

| Hyperscaler AI capex in 2026 | ~$700 billion |

| New data center capacity coming online (2026-2030) | ~100 gigawatts |

The Nuclear Renaissance

Here is the problem that solar and wind create for data centers: they don't run at night and don't run when the weather is calm. Data centers need electricity 24 hours a day, seven days a week, regardless of conditions. This requirement has placed what analysts are calling a "scarcity premium" on baseload power, particularly nuclear, which is the only large-scale carbon-free source that runs continuously.

The result has been a dramatic re-rating of nuclear-heavy power producers.

Constellation Energy (CEG) operates the largest nuclear fleet in the United States, producing roughly 10% of all carbon-free electricity in the country. When it was spun off from Exelon in February 2022, it debuted at roughly $53 per share. As of late March 2026, it trades near $282, a roughly 430% gain in four years. The stock hit an all-time high of $402.95 in October 2025 before consolidating as regulatory concerns around "behind-the-meter" deals emerged. For full year 2025, Constellation reported Adjusted Operating Earnings of $9.39 per share. In the most recent PJM capacity auctions, the company secured approximately $2.2 billion in highly visible, high-margin revenue through locked-in capacity agreements.

Vistra Corp (VST) is the largest unregulated power producer in the United States, combining a 6,400-plus megawatt nuclear fleet with natural gas and battery storage assets. The stock has increased over 600% since 2021. For 2025, Vistra hit the high end of its guidance with adjusted EBITDA of roughly $5.9 billion. Looking into 2026, the company issued midpoint guidance of $7.2 billion, a surge driven by record-high PJM capacity prices and integration of recent acquisitions. Vistra has long-term power supply agreements with Amazon Web Services and Meta.

NRG Energy (NRG) was up nearly 80% by mid-November 2025, making it one of the best-performing stocks in the S&P 500, a figure that outpaced Nvidia over the same period according to Charles Schwab.

How Capacity Auctions Became the Market Mechanism

One of the less-understood dynamics driving utility stock performance is not just power demand itself but the capacity market structure that determines how that demand gets priced.

PJM Interconnection, the grid operator covering 13 states across the mid-Atlantic and Midwest and home to the largest concentration of US data centers, holds annual auctions to secure future power supply. Utilities that clear capacity in these auctions lock in revenue commitments years in advance at whatever price the auction clears.

In recent auctions, capacity prices cleared at record highs, up to $333 per megawatt-day, due to supply tightness and the retirement of fossil-fuel plants. Constellation cleared nearly 18,000 megawatts in these auctions, creating what analysts describe as a "floor" for its earnings through the coming years.

Vistra also benefited directly, as PJM capacity prices hitting their federally approved caps created a multi-billion dollar tailwind for its Eastern fleet. The auction mechanism turns future AI power demand into current utility earnings visibility, which is a large part of why institutional investors began repricing these stocks as growth names rather than defensive income plays.

The Traditional Regulated Utilities

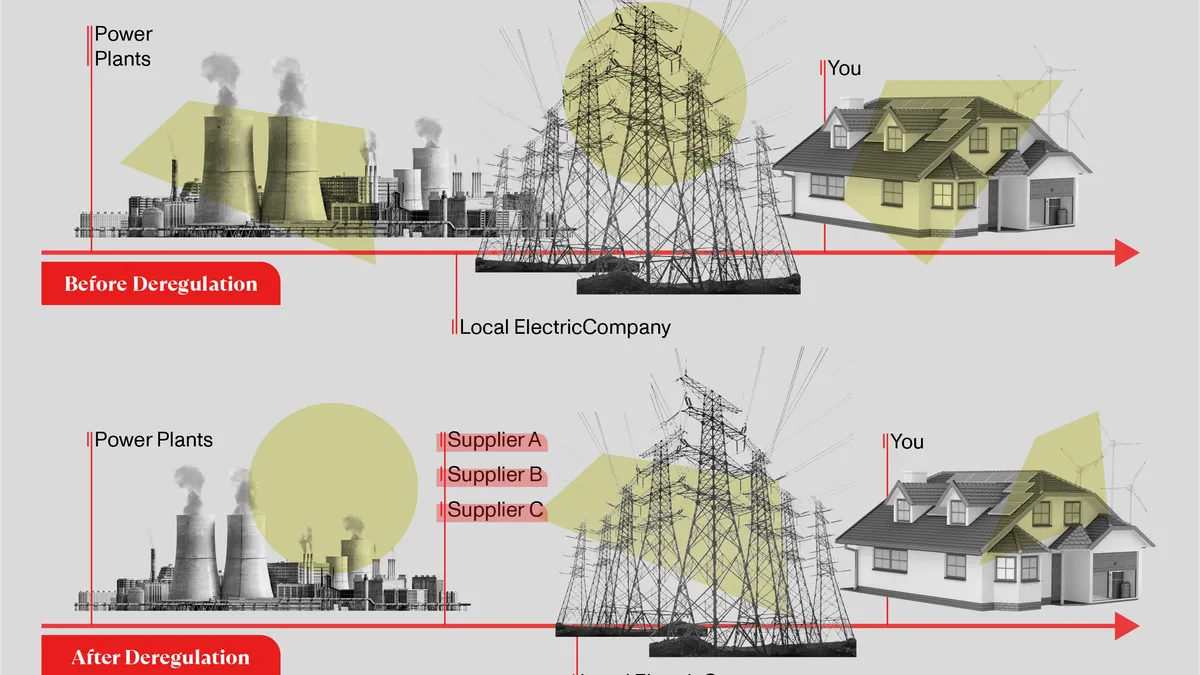

Not all utility winners are nuclear-heavy competitive power producers. Traditional regulated utilities, the kind that own transmission lines and serve residential customers, are also benefiting, though through a different mechanism.

Regulated utilities earn returns on the capital they deploy to build infrastructure. When AI drives demand for massive new transmission lines, substations, and power plants, regulated utilities with aggressive capital investment programs see their rate base, and their permitted earnings, grow substantially.

Dominion Energy has a $50 billion capital investment plan covering 2025 through 2029, with the bulk going to Dominion Energy Virginia. The company targets 5% to 7% annual earnings-per-share growth based on 2025 levels, supported by that investment program.

Entergy is planning $41 billion in investment between 2026 and 2029 on new generation capacity and infrastructure. The company has signed power purchase agreements with NextEra Energy for up to 6.2 gigawatts of renewable energy and storage capacity. It has secured data center deals with Amazon, Alphabet, and Meta, and projects more than 8% compound annual earnings-per-share growth through 2029.

Both companies highlight something important about the regulated utility model in the AI era: capital spending on grid infrastructure is not a cost, it is the product. The more a utility is required to build, the more it is permitted to earn.

The Risks That Come with a Growth Re-Rating

The shift from defensive income stock to growth stock comes with complications that dividend investors did not originally sign up for.

- Valuation stretch. Vistra's trailing price-to-earnings ratio reached 58 times before the forward earnings estimate compression that AI growth is expected to deliver. Constellation's stock fell roughly 30% from its October 2025 high before partial recovery, illustrating how quickly sentiment can reverse even when the underlying thesis is intact.

- Regulatory risk on behind-the-meter deals. There is ongoing litigation and regulatory debate over whether direct deals where a data center connects to a power plant, bypassing the broader grid, unfairly shift grid maintenance costs onto residential ratepayers. If regulators restrict these arrangements, the premium pricing some utilities have secured for AI customers becomes more complicated.

- Cyclical earnings volatility. Vistra's Q3 2025 earnings dropped 66.7% year-over-year and revenue fell 20.9%, reflecting cyclical pressures in power markets. The forward earnings story is strong, but the quarterly path is not straight.

- Operational risk. Nuclear plants are aging infrastructure. Unexpected outages can force a utility to buy expensive replacement power on the open market to fulfill supply commitments, creating significant cost exposure at exactly the wrong moment.

- Demand forecast overstatement. Constellation CEO Joe Dominguez and Vistra CEO James Burke both warned in 2025 that data center demand projections may be overstated by three to five times in some jurisdictions as developers scout projects around the country before committing to sites. Not every announced data center gets built. If a significant portion of projected demand does not materialize, utilities that have already locked in infrastructure investment will face the cost of that overbuilding.

What This Means for Investors

The 15.9% earnings growth forecast for 2026 reflects a genuine structural shift in how the power sector operates. Morningstar projects that top utilities could deliver 8% to 10% annual total returns through 2026 and 2027, combining earnings growth with dividend income, a profile that has historically been rare for the sector.

The sector's transformation from a defensive income play into what Charles Schwab's analysts have described as the "picks and shovels" play of the AI era is a real re-rating, not a temporary sentiment trade. The physical infrastructure that AI depends on, reliable power delivered continuously at scale, is something utilities provide and that the market cannot quickly replicate.

The risk is equally real. These stocks now carry valuation multiples and earnings volatility that traditional utility investors did not price into their models. Investors who bought utilities for their 4% dividend yields and predictable low-single-digit earnings growth are now holding companies with the risk profile of infrastructure growth stocks.

Whether that trade-off works depends on how much AI power demand actually materializes, how regulators handle the pricing conflicts between data center customers and residential ratepayers, and whether nuclear's reliability premium holds as the broader grid adds more flexible capacity over time.

Wrap up

The "boring" utility sector became the AI era's most surprising beneficiary because the physical constraints of the technology were not about software or chips but about electricity. Every model trained, every inference run, and every data center cooled requires continuous power at a scale the existing grid was never designed to provide.

Utilities that own reliable baseload generation, operate in demand-constrained markets, or have the capital investment capacity to build new infrastructure at scale have been repriced accordingly. The 15.9% growth forecast for 2026 is the earnings manifestation of a thesis that the equity market began pricing in years earlier.

The question for the years ahead is not whether AI will need power, but whether the grid can be built fast enough, at an acceptable cost to all ratepayers, to meet it.

Frequently Asked Questions

Why are utility stocks performing so well in 2025 and 2026?

Artificial intelligence data centers require massive amounts of continuous, reliable electricity, creating unprecedented demand growth for power companies. The Morningstar US Utilities Index rose 19% in 2025 and has surged 70% from its late 2023 low. New 2026 forecasts project 15.9% earnings growth for global infrastructure companies, compared to historical low-single-digit averages.

What is the nuclear renaissance in energy stocks?

Data centers need 24/7 power, which intermittent renewables like solar and wind cannot reliably provide alone. This has created a scarcity premium for baseload nuclear power. Constellation Energy, which operates the largest US nuclear fleet, has seen its stock rise roughly 430% since its 2022 spinoff. Vistra Corp, the country's largest unregulated power producer, has risen over 600% since 2021.

How does AI actually drive utility earnings growth?

AI data centers consume enormous electricity continuously, and utilities earn returns on the capital they deploy to build generation and transmission infrastructure to meet that demand. In regulated markets, utilities earn permitted returns on infrastructure investment. In competitive markets like PJM, capacity auction prices have hit record highs as supply tightness drives up the price utilities receive for future power commitments.

What are the risks of investing in utility stocks now?

Key risks include stretched valuations after significant run-ups, regulatory disputes over whether direct data center power deals shift costs to residential ratepayers, cyclical earnings volatility in power markets, aging nuclear infrastructure, and the possibility that data center demand projections are overstated. Both Constellation and Vistra CEOs warned in 2025 that developer demand forecasts may overstate actual build-out by three to five times in some markets.

Which utility companies are most exposed to the AI power demand theme?

The most directly exposed companies include Constellation Energy for its nuclear fleet and capacity auction position, Vistra Corp for its nuclear and gas generation with hyperscaler contracts, and NRG Energy for its data center power supply strategy. Traditional regulated utilities with aggressive capital investment programs, including Dominion Energy and Entergy, also benefit through their rate base growth model. This is informational only and not a recommendation to buy or sell any security.

Will utility earnings growth continue beyond 2026?

Morningstar projects 8% to 10% annual total returns for top utilities in 2026 and 2027, supported by robust earnings and dividend growth. Goldman Sachs projects data center power demand to grow 160% by 2030. However, earnings growth will depend on how much AI infrastructure is actually built, how regulatory frameworks evolve, and whether supply additions eventually moderate the capacity price premiums that are currently driving margins.

Related Articles